Powered for What

The SHASTA topline is days away, and the market may grade it on a number the trial was never built to prove. Here is the distinction to hold before the headline hits.

Robert Toczycki, JD, MBA

bioboyscout.com

bioboyscout@gmail.com

847.227.7909

X: @BioBoyScout

A pivotal readout is coming for Redemplo in severe high triglycerides, the SHASTA-3 and SHASTA-4 topline, expected within days, with full data at a heart conference at the end of August. Before it lands, it is worth separating what the trial was designed to measure from what the market has decided to judge it on, because those are not the same thing, and the gap between them is where the stock is most likely to be mispriced in the first hour after the results.

What the trial is built to show

One piece of vocabulary makes the whole thing clear, so here it is in plain terms. When statisticians say a trial is powered to prove something, they mean it was built big enough, with enough patients and enough time, to give a reliable yes-or-no answer on that specific question. A trial can measure a hundred things, but it is only powered to prove the one or two it was sized around. Power depends largely on how often the event happens and on how many patients are enrolled: when an event is uncommon, even a drug with a substantial effect may require thousands of patients or years of follow-up before statistical significance can be demonstrated. Measuring something is not the same as being able to prove it, and that single distinction is the entire point of this note.

The primary job of this trial is triglyceride reduction, and on that measure the bar is not really in doubt. Investors look for something above roughly 60 to 70 percent. The earlier SHASTA-2 study already delivered about 74 percent, and the main competing drug has shown triglyceride reductions in a comparable neighborhood, roughly 55 to 72 percent across its trials. Triglyceride lowering is the mechanism, it is what the drug is designed to do, and it is what this trial is powered to demonstrate. On the thing the trial was built to prove, expectations are high and, by most reckoning, likely to be met.

What the market has decided to grade

The number investors are actually fixated on is different. It is the reduction in acute pancreatitis events, the dangerous real-world consequence of very high triglycerides. The benchmark in everyone’s mind is the competitor’s headline of an 85 percent reduction in those events. That figure, worth understanding, came from a trial run in a pancreatitis-prone population and built around pancreatitis events, not from a triglyceride-sized study like this one, which is precisely why it makes an unfair yardstick for SHASTA. The reflex on results day, then, will be to compare Redemplo’s pancreatitis number against that bar and grade the drug a winner or a loser on the spot.

Here is the problem with that reflex, and it is not a subtle one. Pancreatitis is not an afterthought in these trials. It is a formally tracked outcome, the studies count pancreatitis events, related hospitalizations, and emergency visits, and they were described from the start as designed to look at whether the drug lowers both triglycerides and the rate of pancreatitis. The events are measured, in other words, and measured carefully.

What the trial can prove is a different matter, and this is the crux. The trial was sized around triglycerides, roughly 750 patients over a single year, which is enough to give a clean answer on triglyceride lowering. Pancreatitis, though, is a rare event. In a group that size over one year, only a small number of pancreatitis cases will occur at all, and that is simply too few to produce a statistically reliable result, the kind that clears the bar scientists and regulators treat as proof. The drug can genuinely reduce pancreatitis and the trial can still be unable to prove it to that standard, purely because it was not built to. Measured, yes. Powered to prove, no. Much of the print-day risk lives in that gap.

There is a clean piece of evidence that this is deliberate, and it is the most convincing detail of all. Arrowhead built a separate trial, SHASTA-5, for the specific purpose of proving a reduction in pancreatitis, enrolling only high-risk patients who have already suffered multiple pancreatitis attacks, and running for up to three years rather than one. A company does not construct a dedicated, years-long trial to prove something its main trials could already prove. The existence of SHASTA-5 is the clearest possible confirmation that SHASTA-3 and SHASTA-4 were never meant to settle the pancreatitis question. That job was handed to a different study, on purpose.

Why the distinction matters on print day

Follow that through to print day. If the pancreatitis numbers do not reach that bar of statistical proof, the quick, headline-reading reaction will be that the drug missed. That reading would be wrong, or at least badly incomplete, because you cannot miss a bar the trial was never built to clear. A pancreatitis result that falls short of formal proof, in a trial sized for triglycerides, is a feature of how the study was designed, not a verdict on whether the medicine works. What actually matters in that case is the size of the pancreatitis reduction and which direction it points, not whether it crossed a proof threshold the trial was never meant to reach.

The medical reality and the market reaction are likely to split here, and even the Wall Street analysts have quietly admitted it, noting that doctors will lean on the established biology, lower triglycerides mean fewer pancreatitis attacks, even where one trial cannot prove the reduction to a statistical certainty. Doctors treat the mechanism. Headlines grade the statistics. Those are two different audiences drawing two different conclusions from the very same result.

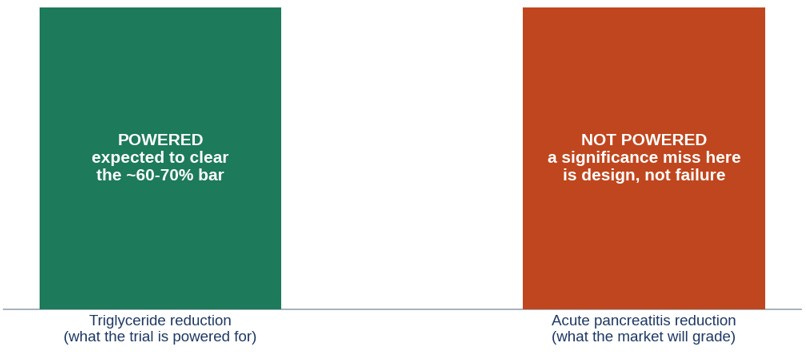

Figure 1: Powered to prove one thing, graded on another

The trial is sized to demonstrate triglyceride reduction, where the bar is expected to be cleared. The market will grade it on acute pancreatitis reduction, an outcome the trial is not powered to prove statistically. A significance miss on the second is a design feature, not a drug failure. Illustrative framing of the powering distinction.

How to read the result without being whipsawed

Hold three cases in advance, so the headline does not set the interpretation for you. If triglycerides clear the bar and pancreatitis shows a large reduction that also reaches significance, that is an unambiguous win, and the market will treat it as one. If triglycerides clear the bar and pancreatitis reduction is large in magnitude but short of significance, the headline may read negative for an hour, and it should not, because that is the trial doing exactly what a triglyceride-powered study does with a rare event. The number to read in that case is the size and direction of the pancreatitis effect, not whether it earned a stamp of statistical proof. Only the third case, a triglyceride result that falls short of the expected range, would be a genuine disappointment on the terms the trial was actually built to test.

The tie to the larger thesis

This is the same distinction that runs through everything I have written on this company. Separate the question a study was designed to answer from the question the market wants answered, and the mispricing usually lives in the gap. On results day the gap will sit between a triglyceride result the trial can prove and a pancreatitis result it cannot, and the first reaction is likely to judge the second as if the trial had been built to settle it.

Chess has a precise word for this situation. A player can hold a winning position, material up, the outcome not in doubt to anyone who actually reads the board, while the scoreboard still shows the game as undecided, because checkmate has not yet been forced. The impatient spectator glances over, sees no mate, and assumes nothing has happened. The player knows the win is already on the board and simply has not been delivered yet. Lower the triglycerides and you have the winning position. The forced mate, statistical proof on pancreatitis, was assigned to a different game, SHASTA-5, on purpose.

When the results land, do not ask whether Redemplo delivered checkmate in a trial that was never set up to force one. Ask whether it is winning. On triglycerides, it almost certainly is, and a winning position converts. The market may spend a headline or two confusing an undelivered mate for a lost game. That confusion is not a verdict on the drug. It is the buying opportunity.

A Note on Supporting Independent Research

If this note has been valuable to you, whether it shaped your thinking, validated your conviction, or simply saved you the time of doing this work yourself, a voluntary contribution is genuinely appreciated and directly funds the next paper.

For individual investors and readers

Any amount you feel reflects the value you received is welcome and meaningful. A contribution in the range of what you might pay for a single premium research report is a thoughtful gesture that makes a real difference.

For family offices, investment funds, hedge funds, and research platforms

This paper is the caliber of work that institutional research desks bill significant retainers to produce. If your team referenced it, distributed it internally, or used it to inform a position, a suggested contribution of $1,000 reflects the professional value of the analysis, though any amount is meaningful. Your support makes it possible to continue publishing at this level without a paywall that limits the reach of the ideas. If your organization requires an invoice to process a payment, please reach out directly at bioboyscout@gmail.com and one will be provided promptly.

There is no obligation and no expectation. This is purely a thank you for work that meant something to you.

Zelle: (847) 227-7909

Thank you for reading, and for being part of a community that takes this thesis seriously.

— Robert Toczycki | BioBoyScout

Important Risks, Disclosures, & Disclaimers

The author, Robert Toczycki (aka BioBoyScout), certifies that:

all views expressed in this note accurately reflect his personal opinions about the topic discussed;

he was not compensated in any form for producing this note; and

he has not received and does not receive compensation from Arrowhead Pharmaceuticals.

This note reflects the author’s personal opinions, is for informational purposes only. It does not constitute investment advice, a solicitation to buy or sell securities, or a guarantee of future results. The author holds a long position in Arrowhead common stock. Arrowhead Pharmaceuticals (ARWR) is a publicly traded company; investments in its shares involve material risks, including the risk of total loss.

About the Author

Robert Toczycki is an independent analyst and registered US Patent Attorney with a JD, an Executive MBA completed at the top of his class, and a BS in Mathematics and Computer Science from the University of Illinois at Urbana-Champaign. He has a deep passion for financial analysis, particularly identifying valuation discrepancies and demonstrating them through rigorous, data-driven research and solid analytics.

Comments or questions: bioboyscout@gmail.com.

Copyright © 2026, BioBoyScout. All Rights Reserved.