Originally published March 26, 2026, as a BioBoyScout white paper. Republished here on Substack with full content, embedded charts, and downloadable PDF. — Robert

A Deep-Dive Investment Thesis on Redemplo vs. Tryngolza, the Structural Case for RNAi Superiority, Underpenetrated Triglyceride Markets, and Why the Floor Scenario for Arrowhead is Already Compelling

Robert Toczycki, JD, MBA

bioboyscout.com

bioboyscout@gmail.com

847.227.7909

X: @BioBoyScout

Executive Summary

On March 25, 2026, Ionis Pharmaceuticals announced a dramatic repricing of Tryngolza (olezarsen), slashing its annual wholesale acquisition cost (WAC) from $595,000 to $40,000, a 93% price reduction effective April 1, 2026. The announcement was framed as a broad-access initiative ahead of the drug’s anticipated June 2026 FDA PDUFA date for the larger severe hypertriglyceridemia (sHTG) indication.

On the surface, this appears threatening to Arrowhead Pharmaceuticals (ARWR) and its approved APOC3-targeting RNAi therapy, Redemplo (plozasiran), which carries a list price of $60,000. The market’s initial read, that Ionis has drawn first blood in a price war, misses several critical structural and clinical realities that favor Arrowhead over the medium and long term.

This analysis makes the following case:

Ionis’s $40,000 price point is a defensive maneuver, not a position of strength, it reflects the company’s need to compete before Redemplo captures further market share.

Redemplo’s clinical and pharmacological profile is meaningfully superior to Tryngolza’s, particularly on dosing convenience, depth of triglyceride reduction, and safety.

Even in a scenario where both drugs succeed commercially, the sHTG market is so large that Arrowhead wins decisively, the two-winner case is the floor, not the ceiling.

Phase 3 SHASTA-3/4 data, expected in Q3 2026, is likely to establish Redemplo as the standard of care in sHTG, supported by FDA Breakthrough Therapy designation.

Payer dynamics will ultimately favor the drug with the stronger clinical evidence and the better dosing schedule, and that is Redemplo.

The conclusion is straightforward: Ionis has opened the first chapter of a commercial battle it is structurally ill-positioned to win. Arrowhead enters this contest with a superior molecule, a smarter pricing strategy, and the most important clinical readouts of 2026 still ahead of it.

I. The Ionis Price Cut: What It Is and What It Isn’t

The Announcement

Ionis announced that Tryngolza’s WAC for the sHTG indication would be set at $40,000, a fraction of the $595,000 price it carries for the rare FCS indication. The company framed this as a commitment to broad access for the larger patient population, with a June 30, 2026 PDUFA date for the sHTG label expansion.

Notably, this price point came in above analyst expectations. Stifel and William Blair had previously modeled $10,000 to $20,000 as the expected net price for Tryngolza in sHTG. At $40,000 WAC, net pricing after rebates may land around $25,000 to $32,000, directionally higher than what the Street had feared. That detail matters: Ionis drew a price floor, not a race to zero.

A Defensive Move, Not Aggression

Ionis’s price cut should be read as a reaction to competitive pressure from Redemplo, not an act of market aggression from a position of strength. The evidence is fairly clear:

Redemplo launched at $60,000 in FCS and immediately began capturing patients, including documented switchers from olezarsen.

Arrowhead management reported approximately 100 Redemplo prescriptions in just the first 10 weeks of launch, with some patients actively switching away from Tryngolza.

Ionis recognizes that if Redemplo secures the sHTG indication with superior label language, the market dynamic would decisively shift before Tryngolza could establish a foothold.

By cutting the sHTG price sharply now, Ionis is attempting to pre-anchor payer expectations before Arrowhead’s Q3 Phase 3 data arrives.

This is the behavior of a company trying to protect turf, not a company confident in its product’s ability to compete on merit.

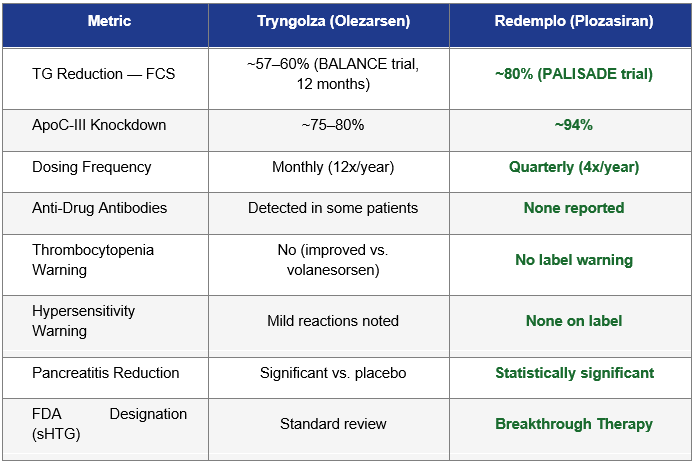

II. Clinical Differentiation: Redemplo’s Decisive Advantages

Mechanism of Action: siRNA vs. ASO

Both Tryngolza (olezarsen) and Redemplo (plozasiran) target ApoC-III, the key regulator of triglyceride metabolism. The modality distinction, however, is clinically meaningful:

Tryngolza is a GalNAc-conjugated antisense oligonucleotide (ASO), requiring monthly subcutaneous injections.

Redemplo is a GalNAc-conjugated small interfering RNA (siRNA), the same RNAi platform behind Alnylam’s blockbuster inclisiran, requiring only once-quarterly injections (or even semi-annual dosing in some protocols).

The dosing difference is not trivial. Monthly injections require 12 healthcare encounters per year; quarterly injections require only four. For a chronic condition managed lifelong, the adherence and patient experience gap is substantial. In payer value frameworks, reduced injection burden translates directly into improved compliance rates, fewer hospitalizations, and stronger cost-effectiveness arguments.

Depth of Triglyceride Reduction

On the primary endpoint that matters, how far triglycerides are reduced, Redemplo has demonstrated a consistent and meaningful advantage over Tryngolza in cross-trial comparisons:

Note: Cross-trial comparisons carry inherent limitations due to differing patient populations, baseline TG levels, and trial designs. These figures are illustrative of directional advantages and should not be treated as head-to-head data.

The Pancreatitis Endpoint Is Arrowhead’s Sword

Arrowhead’s clinical strategy is particularly astute: management has consistently framed Redemplo not primarily as a triglyceride drug, but as a pancreatitis prevention drug. This is not marketing spin. Acute pancreatitis (AP) is the primary clinical consequence of sHTG, and it drives the majority of direct and indirect costs associated with the condition.

Arrowhead’s SHASTA-3/4 studies include a pancreatitis endpoint. If Phase 3 data shows a statistically significant reduction in AP events, which the Phase 2 SHASTA-2 data strongly suggests is likely, given that most patients treated with plozasiran achieved TG levels below the 500 mg/dL pancreatitis risk threshold, Redemplo’s label will reflect a hard clinical outcome that payers and prescribers can directly value.

A drug that prevents pancreatitis hospitalizations, average cost exceeding $25,000 per event, is economically compelling even at a $60,000 annual price point. Tryngolza, entering the sHTG space at $40,000 without a pancreatitis label (at least initially), faces a steeper challenge in demonstrating equivalent economic value to payers.

FDA Breakthrough Therapy Designation

In December 2025, the FDA granted Breakthrough Therapy designation to plozasiran for sHTG. This designation, reserved for drugs showing substantial improvement over available therapies on clinically significant endpoints, carries significant practical advantages:

More intensive FDA guidance during development, reducing regulatory risk.

Eligibility for rolling review, potentially accelerating the approval timeline.

A powerful signal to payers that the FDA views plozasiran as a clinically meaningful advance over what currently exists, including Tryngolza.

Ionis did not receive Breakthrough Therapy designation for Tryngolza in sHTG. That asymmetry is commercially and regulatorily significant.

III. The Two-Winner Case: Why Even the Floor Scenario Is Compelling for Arrowhead

Much of the initial market reaction to the Tryngolza price cut assumes a zero-sum dynamic: that Ionis’s commercial gain is Arrowhead’s loss. This framing fundamentally misunderstands the size and structure of the sHTG market. The more important analytical exercise is not “who wins the market” but rather “what does Arrowhead’s outcome look like even if both drugs succeed?” The answer, modeled carefully, is still transformative.

The Market Is Exceptionally Large

Arrowhead estimates approximately 3 million U.S. patients with triglycerides above 500 mg/dL, including roughly 1 million above 880 mg/dL, the range associated with the highest acute pancreatitis risk. To put this in context:

The entire FCS patient population, the existing approved indication for both drugs, numbers only around 3,000 to 5,000 patients in the U.S. The sHTG addressable market is approximately 600 to 1,000 times larger.

Current treatment penetration in sHTG is extremely low. Fibrates and omega-3 fatty acids are the standard of care but frequently fail to bring triglycerides below dangerous thresholds. There is essentially no approved, targeted pharmacotherapy for this patient population today.

Physician awareness of sHTG as a treatable disease is growing but remains low. Both Ionis and Arrowhead will need to invest heavily in market education, and that education benefits both drugs.

The sHTG population is not geographically or demographically concentrated. It spans primary care, endocrinology, cardiology, and gastroenterology, meaning no single company can dominate the prescriber landscape in the near term regardless of commercial effort.

In short, this is not a market where two drugs are fighting over a fixed pool of 10,000 patients. It is a market where the primary challenge is reaching a vastly underpenetrated population of millions.

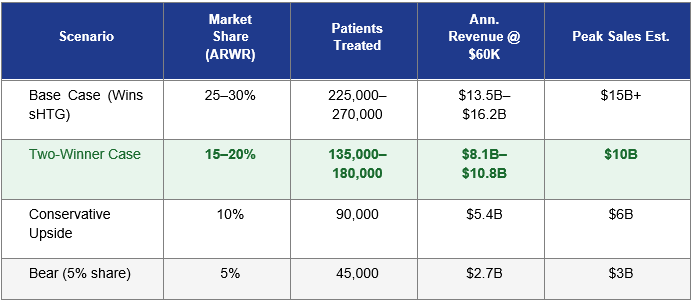

Modeling the Two-Winner Scenario

The following table models Arrowhead’s revenue potential across a range of sHTG market share scenarios, assuming a 900,000-patient primary addressable market (patients above 500 mg/dL most likely to be treated with injectable therapy) and a $60,000 annual WAC with ~80% net pricing realization:

Assumes 900,000 primary addressable patients in the U.S., $60,000 WAC, ~80% net price realization (~$48,000 net). Market penetration is assumed to build over 5–7 years post-approval. Revenue figures represent annual peak, not Year 1. These are illustrative estimates, not guidance.

The highlighted row, the Two-Winner Case, is the analytical floor for a thesis on Arrowhead. In this scenario, Tryngolza and Redemplo each secure meaningful market share, with Ionis’s price advantage helping it reach certain cost-sensitive patients while Redemplo commands a premium among patients where clinical performance and dosing convenience are prioritized. Even at 15–20% share, Redemplo generates $8B to $11B in peak annual revenue, a number that, discounted back, implies a significantly higher share price than where ARWR currently trades.

Historical Precedent: Large Markets Accommodate Multiple Winners

The history of pharmaceutical markets with large, underpenetrated patient populations consistently demonstrates that clinical differentiation and market share coexist comfortably. Consider three analogous competitive dynamics:

PCSK9 inhibitors (Repatha vs. Praluent): Both Amgen’s Repatha and Regeneron/Sanofi’s Praluent launched as competitors in the LDL-lowering market. Despite years of head-to-head competition and significant price pressure, both drugs have achieved blockbuster revenues. The market for LDL management was large enough and underpenetrated enough that two winners emerged, with outcomes differentiated primarily by payer contracts and dosing schedule rather than one drug eliminating the other.

GLP-1 receptor agonists (Ozempic vs. Victoza vs. Trulicity): The GLP-1 space in diabetes and obesity has sustained four or more commercially successful drugs simultaneously. Market size and physician preference diversity, not competitive exclusion, determined outcomes.

SGLT2 inhibitors (Jardiance vs. Farxiga vs. Invokana): Multiple agents with distinct clinical evidence packages captured distinct payer tiers and prescriber preferences. The market did not choose a single winner; it allocated patients across products based on clinical differentiation and contracting.

In each of these analogues, the market was large, underpenetrated, and growing, exactly the profile of sHTG today. The lesson is consistent: in markets of sufficient scale, the question is rarely “which drug wins” but rather “how big can each drug become?” For Arrowhead, even a conservative answer to that question represents a fundamental re-rating opportunity.

Why Arrowhead Still Wins the Two-Winner Market

Even stipulating a two-winner outcome, the most cautious realistic scenario for Arrowhead investors, several structural factors ensure that Redemplo captures the more valuable half of the market:

Patient stratification by severity: The highest-risk sHTG patients, those with triglycerides above 880 mg/dL and frequent AP hospitalizations, are also the patients where maximum TG reduction is most clinically important. Redemplo’s deeper knockdown (~80% vs. ~60%) is disproportionately valuable in precisely this highest-acuity, highest-revenue tier.

Specialist vs. generalist prescriber dynamics: Endocrinologists and metabolic disease specialists, who will manage the most complex sHTG cases, tend to prioritize efficacy over price when outcomes are meaningfully differentiated. Redemplo’s profile is built for this audience.

Pancreatitis label as a market separator: If Redemplo achieves a pancreatitis outcomes label and Tryngolza does not (at least initially), payers managing hospitalization costs will have a direct economic incentive to tier Redemplo favorably in the highest-risk patient segment, regardless of acquisition price difference.

Dosing adherence over time: Chronic disease markets increasingly reward drugs with better adherence profiles because payers know that non-adherence drives total cost of care up. A quarterly injection that patients actually keep coming back for is worth more than a monthly injection that drives discontinuation at year two.

In the two-winner scenario, Ionis likely captures a larger share of cost-sensitive, lower-severity, primary-care-managed patients, while Arrowhead captures the specialist-managed, highest-acuity tier. That split would favor Arrowhead on revenue per patient and on the durability of its market position.

IV. Pricing Strategy: Arrowhead Is Playing the Right Game

The $60,000 Anchor Was Deliberate

Arrowhead CEO Chris Anzalone explained the $60,000 pricing decision at the JPMorgan Healthcare Conference in January 2026: the company chose to avoid pricing at many hundreds of thousands of dollars in FCS because it views sHTG, not FCS, as the primary commercial opportunity. A consistent one-price model across both indications simplifies payer contracting and signals that Arrowhead built its economics around the mass market from the outset.

This pricing philosophy is sophisticated. By not gouging on FCS (where earlier volanesorsen-era pricing set expectations for ultra-high specialty drug pricing), Arrowhead has positioned itself as a value-oriented partner to payers entering the sHTG space. That relationship capital has real worth when formulary negotiations begin.

The $40,000 vs. $60,000 Gap Is Narrower Than It Looks

On WAC, Ionis has a $20,000 annual price advantage. In practice, that gap narrows substantially:

Mandatory Medicaid rebates and commercial contract rebates will reduce both drugs’ net prices. Ionis’s deep WAC cut likely reflects an already-expected low net price after rebates.

If Redemplo’s Phase 3 data shows superior pancreatitis outcomes, payers will weight the cost-effectiveness calculation on outcomes prevented, not just acquisition cost.

The $20,000 WAC delta is approximately the cost of one emergency room visit or partial pancreatitis hospitalization. A drug that prevents even one additional AP event annually per patient more than Tryngolza closes the price gap entirely from a payer perspective.

Arrowhead’s quarterly dosing reduces administration cost and care coordination burden, partially offsetting the acquisition price difference.

V. The SHASTA-3/4 Catalyst: Why Q3 2026 Is the Inflection Point

What Arrowhead Expects

Arrowhead has completed enrollment in its SHASTA-3, SHASTA-4, and MUIR-3 Phase 3 studies, with approximately 2,200 patients enrolled across 24 countries. Primary endpoint data, triglyceride reduction at 12 months, is expected in Q3 2026, followed by an sNDA filing in Q4 2026 and a potential sHTG label expansion in 2027.

The Probability of Success Is High

Phase 2 SHASTA-2 data showed plozasiran reduced TG below the 500 mg/dL AP risk threshold in most patients, a clean and convincing mechanistic demonstration.

The primary endpoint (TG reduction at 12 months) is the same endpoint that drove FDA approval for Tryngolza in FCS. Arrowhead is targeting a well-validated regulatory path.

FDA Breakthrough Therapy designation implies the agency has already reviewed preliminary evidence suggesting substantial improvement over existing therapies.

Arrowhead management has characterized the competitive differences as “quite stark” and specifically called out deeper TG reduction and a cleaner safety profile.

A failed Phase 3 outcome, while always possible, would require plozasiran to have dramatically underperformed its Phase 2 profile in a much larger and more diverse patient population, a scenario not supported by the existing clinical evidence.

What a Positive Readout Means Commercially

Redemplo becomes the only sHTG drug with both a robust triglyceride reduction label AND a pancreatitis outcomes claim.

Arrowhead’s sNDA would include a clean safety profile, no immunogenicity, and a once-quarterly dosing schedule, all of which become label differentiators.

Breakthrough Therapy designation accelerates FDA review, meaning a potential 2027 sHTG approval that is competitive with or ahead of Tryngolza’s penetration timeline.

Institutional investors awaiting binary risk resolution will have clear line-of-sight to a blockbuster commercial opportunity in a market now proven to support two $40K–$60K price points simultaneously.

VI. The Broader Arrowhead Thesis Is Intact

Platform Value Beyond sHTG

ARWR’s investment thesis extends well beyond the APOC3 franchise. Tryngolza’s price cut is relevant to the plozasiran/sHTG chapter of the story, but Arrowhead’s pipeline includes multiple high-value programs:

ARO-INHBE (obesity/metabolic): A potentially differentiated siRNA targeting INHBE for weight loss, with early Phase 2 data expected in 2026.

ARO-ALK7 (obesity): A complementary obesity program providing platform diversification into the largest pharma market.

ARO-MAPT (Alzheimer’s/tauopathies): Early CNS data expected in late Q3 or Q4 2026, representing a massive unmet need and potential platform extension into neurology.

ARO-DIMER-PA: Initial clinical data expected in the second half of 2026, expanding the pipeline into rare disease.

No single competitive development in sHTG changes the platform-level value of Arrowhead’s RNAi delivery infrastructure, its manufacturing capabilities, or its pipeline optionality. The company holds approximately $920 million in cash, expects to approach breakeven in 2026, and is self-funding multiple Phase 3 programs simultaneously.

FCS Commercial Momentum Continues

In the FCS market, where Redemplo is already approved and commercially launched, the competitive dynamic is shifting in Arrowhead’s favor. Early launch metrics show approximately 100 prescriptions in the first 10 weeks, with documented patient switching from Tryngolza. Prescribers are choosing Redemplo’s quarterly dosing and superior TG reduction profile even at a comparable or slightly higher price point.

This real-world switching behavior is arguably the most meaningful competitive data point currently available: it demonstrates that when clinicians and patients are actually making treatment decisions, Redemplo wins.

VII. Risk Factors

A balanced analysis must acknowledge the risks to this thesis:

Phase 3 miss: A failure in SHASTA-3/4 would significantly impair the sHTG commercial case. This remains the primary binary risk.

Payer resistance at $60K: If payers anchor hard to the $40K Tryngolza reference price, Arrowhead may face formulary exclusion or step therapy requirements in some plans.

Label differentials: Tryngolza’s earlier market presence may allow it to capture prescriber habits and patient adherence before Redemplo’s sHTG label arrives.

Ionis price flexibility: If Tryngolza underperforms commercially at $40K, Ionis could cut pricing further, though this would further pressure its own revenues.

Macro headwinds: Drug pricing legislation, IRA negotiation dynamics, or broader macro conditions could compress pharmaceutical valuations regardless of clinical outcomes.

VIII. Conclusion: The Floor Is Already Compelling; the Ceiling Is Higher Still

Ionis Pharmaceuticals’ decision to cut Tryngolza’s price by 93% should be read not as a competitive victory, but as a concession that Redemplo has fundamentally altered the dynamics of the APOC3-targeting space. A company confident in the superiority of its product does not slash its price by $555,000 before a competitor’s Phase 3 data even arrives.

The most important analytical reframe for investors is this: a two-winner outcome in sHTG is not a bad scenario for Arrowhead, it is the floor. The sHTG market is large enough, underpenetrated enough, and structurally complex enough that even a minority share of it represents a multi-billion-dollar revenue stream that is not currently priced into ARWR’s market capitalization. The historical analogues from PCSK9 inhibitors to GLP-1 agonists are unambiguous on this point: in large, growing, underpenetrated markets, clinical differentiation and scale both win.

Arrowhead’s best case, Redemplo capturing 25–30% of sHTG on the strength of a pancreatitis outcomes label, quarterly dosing, and superior TG knockdown, implies peak revenues that would represent a fundamental re-rating of the stock. The worst realistic case, a 10–15% share in a two-winner market, still implies $5B to $8B in annual revenue from a single drug in a single indication, for a company that currently carries a fraction of that in enterprise value.

The Q3 2026 SHASTA-3/4 readout is the most important near-term catalyst for ARWR. If, as the evidence strongly suggests, it confirms plozasiran’s efficacy and safety advantages in the broader sHTG population, the commercial and stock price implications will dwarf today’s noise around Ionis’s pricing action.

Key Investment Thesis Points

The two-winner sHTG market scenario is the floor for Arrowhead, not the ceiling, even at 15% share, Redemplo generates $8B+ in peak annual revenue

Redemplo’s once-quarterly siRNA dosing vs. Tryngolza’s monthly ASO injections is a durable, clinician-valued differentiator that drives adherence and payer preference

~80% TG reduction vs. ~57–60% for Tryngolza represents a clinically meaningful efficacy gap, most valuable in the highest-acuity patients where revenue per patient is highest

FDA Breakthrough Therapy designation for sHTG signals regulatory and clinical confidence in plozasiran’s profile, a signal Tryngolza cannot match

SHASTA-3/4 Phase 3 readout (Q3 2026) is a high-probability positive catalyst; Phase 2 data and enrollment completion both support confidence

Real-world FCS switching from Tryngolza to Redemplo demonstrates genuine prescriber preference even before sHTG approval

Historical analogues (PCSK9, GLP-1, SGLT2) confirm that large underpenetrated markets consistently produce multiple commercial winners

$920M cash position enables independent execution through all key 2026 milestones without dilutive financing pressure

A Note on Supporting Independent Research

These white papers took hundreds of hours to produce. The asset inventory, valuation methodology, bidder analysis, comparable transaction work, acquisition thesis, competitor analysis, supporting charts, and science analytics are the result of deep primary research and is not available in sell-side coverage. Most of the analysis presented represents independent research not published elsewhere. It is being shared freely because the thesis deserves the widest possible audience. Every Arrowhead shareholder benefits from a well-informed market that understands what the data means and what the asset is worth. That is why this paper exists.

If this research has been valuable to you, whether it shaped your thinking, validated your conviction, or simply saved you the time of doing this work yourself, a voluntary contribution is genuinely appreciated and directly funds the next paper.

For individual investors and readers

Any amount you feel reflects the value you received is welcome and meaningful. A contribution in the range of what you might pay for a single premium research report is a thoughtful gesture that makes a real difference.

For family offices, investment funds, hedge funds, and research platforms

This paper is the caliber of work that institutional research desks bill significant retainers to produce. If your team referenced it, distributed it internally, or used it to inform a position, a suggested contribution of $1,000 or more reflects the professional value of the analysis, though any amount is meaningful. Your support makes it possible to continue publishing at this level without a paywall that limits the reach of the ideas. If your organization requires an invoice to process a payment, please reach out directly at bioboyscout@gmail.com and one will be provided promptly.

There is no obligation and no expectation. This is purely a thank you for work that meant something to you.

Zelle: (847) 227-7909

PayPal: paypal.me/bioboyscout

Thank you for reading, and for being part of a community that takes this thesis seriously.

— Robert Toczycki | BioBoyScout

Important Risks, Disclosures, & Disclaimers

The author, Robert Toczycki (aka BioBoyScout), certifies that:

About the Author

Robert Toczycki is an independent analyst and registered US Patent Attorney with a JD, an Executive MBA completed at the top of his class, and a BS in Mathematics and Computer Science from the University of Illinois at Urbana-Champaign. He has a deep passion for financial analysis, particularly identifying valuation discrepancies and demonstrating them through rigorous, data-driven research and solid analytics.