Originally published April 22, 2026, as a BioBoyScout white paper. Republished here on Substack with full content, embedded charts, and downloadable PDF. — Robert

A Deep-Dive Valuation Analysis of ARO-MAPT's Path to Acquisition Across Four Methodologies, Three Phase 1 Scenarios, and a $55 to $150 Billion Range of Outcomes

Robert Toczycki, JD, MBA

bioboyscout@gmail.com

847.227.7909

X: @BioBoyScout

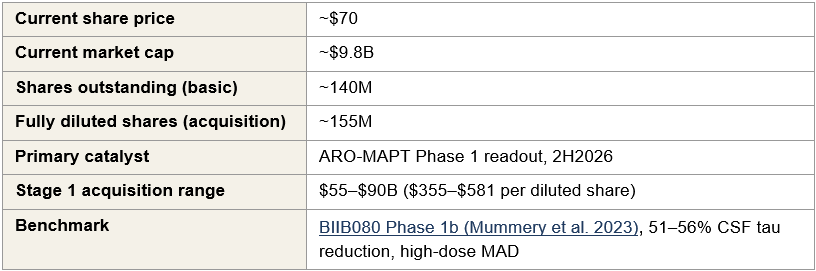

On November 18, 2025, the FDA approved Arrowhead Pharmaceuticals’ first commercial product, Redemplo (plozasiran). In the second half of 2026, Phase 1 data will read out from ARO-MAPT, Arrowhead’s subcutaneous tau-silencing program for Alzheimer’s disease. This readout is the single most consequential re-rating event for Arrowhead’s valuation: positive data validates subcutaneous CNS delivery and converts the company from pipeline biotech to strategic acquisition target. The stock trades at approximately $9.8 billion. This paper argues that number is materially mispriced. A Stage 1 acquisition range of $55 to $90 billion, roughly six to nine times today’s market cap, reflects what a disciplined competitive process produces, with Stage 2 forward optionality of $110 to $150 billion if positive Phase 2 cognitive data follows in 2029 to 2030.

Executive Summary

Arrowhead Pharmaceuticals (ARWR) trades at approximately $9.8 billion. In the second half of 2026, ARO-MAPT, Arrowhead’s subcutaneous tau-silencing program for Alzheimer’s disease, will produce Phase 1 human data.

The quality of that data will force one of three outcomes: probable acquisition in the $55 to $90 billion range (5.6× to 9.2× today’s market cap), meaningful re-rating with licensing as a realistic alternative path, or invalidation of the acquisition thesis bounded by a non-CNS floor at approximately today’s market cap. The asymmetric entry point is today, before the readout.

Key parameters

The three scenarios

Scenario probabilities are the paper’s assessment based on the prior evidence developed in Section I; reasonable alternative weightings produce qualitatively similar conclusions. If positive Phase 1 data does not result in a transaction within 12–18 months, positive Phase 2 cognitive endpoint data in 2029–2030 would open a subsequent valuation window at approximately $110–$150B. Stage 2 is treated as conditional forward optionality rather than a primary scenario.

Why now

The prior evidence base for positive Phase 1 data is substantial: BIIB080 has validated MAPT-silencing as a biomarker-active mechanism in humans; trontinemab has validated TfR1-mediated blood-brain-barrier transcytosis as a delivery route; Arrowhead’s non-human-primate CSF tau reduction data supports translational feasibility. Taken together, this prior evidence makes the weak Phase 1 scenario less probable than the current $9.8 billion valuation implies. Section VI develops the full probabilistic case.

Series context

This paper is the fourth in the BioBoyScout Arrowhead research series. The first, The Needle Wins (March 2026), established that the rapid adoption of GLP-1 auto-injectors has normalized subcutaneous injection as a chronic-disease delivery format, benefiting every commercial-scale RNAi therapeutics company. The second, Redemplo vs. Tryngolza (March 2026), analyzed the competitive dynamics between plozasiran and Ionis’s Tryngolza in the severe hypertriglyceridemia market following Ionis’s 2025 pricing action. The third, The Year of Tau (April 2026), examined the ARO-MAPT program in detail, the non-human-primate CSF tau reduction data, the TfR1-mediated blood-brain-barrier delivery mechanism, and the clinical development plan leading to the Phase 1 readout in 2H2026. Read together, the four papers trace the investment thesis from platform viability to commercial competitive dynamics to clinical catalyst to acquisition outcome.

What this paper establishes

The analysis that follows documents the asset inventory, the four valuation methodologies pharma M&A teams use to triangulate acquisition pricing, the Monte Carlo enterprise value distribution that anchors the Stage 1 range, and the specific acquirer and licensee rationales for Eli Lilly, Roche, Novartis. It commits to specific ranges for each scenario rather than deferring to qualitative conclusions.

Risk note: If ARO-MAPT Phase 1 data does not meet the moderate threshold, the acquisition thesis is invalidated. The downside is bounded by a non-CNS commercial business whose probability-adjusted value sits near today’s market cap. This is a meaningful but not catastrophic downside.

I. The Thesis

Arrowhead Pharmaceuticals trades at approximately $9.8 billion. The central argument of this paper is that this market capitalization underprices a specific and near-term opportunity: in the second half of 2026, Arrowhead’s lead CNS program, ARO-MAPT, will produce Phase 1 data that, depending on its quality, will force one of three distinct outcomes. One of those outcomes is probable acquisition at a valuation multiple of today’s market cap. Another is meaningful re-rating with extended optionality through licensing or delayed acquisition. The third is invalidation of the acquisition thesis, bounded by a non-CNS floor that limits downside. The purpose of this paper is to make the probabilistic case for each outcome.

The Phase 1 readout is the single most consequential event for Arrowhead’s valuation in the next three years.

ARO-MAPT is designed to silence MAPT, the gene that encodes tau protein, by delivering a subcutaneous RNAi therapeutic across the blood-brain barrier using Arrowhead’s TRiM delivery platform. Success means two things simultaneously: validation of tau-silencing as a disease-modifying approach to Alzheimer’s disease, and validation that Arrowhead has built the only subcutaneous CNS-delivery platform in the industry. The first makes ARO-MAPT commercially valuable, and the second makes Arrowhead strategically irreplaceable. No other siRNA company has demonstrated subcutaneous blood-brain-barrier crossing with therapeutic-scale gene silencing in humans. A positive Phase 1 readout converts Arrowhead from a pipeline company with an interesting platform into an acquisition target that strategic acquirers will find difficult to leave untouched.

The data will not be binary.

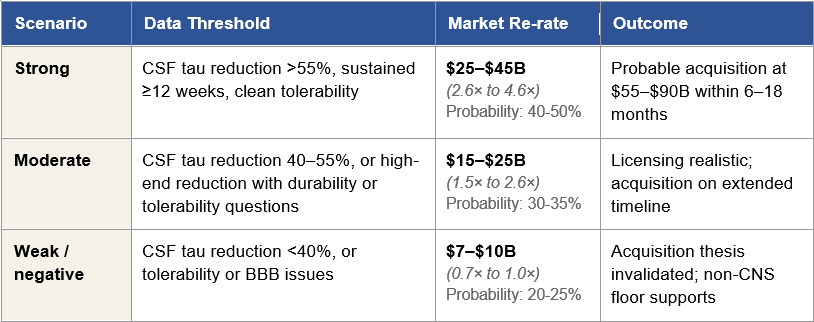

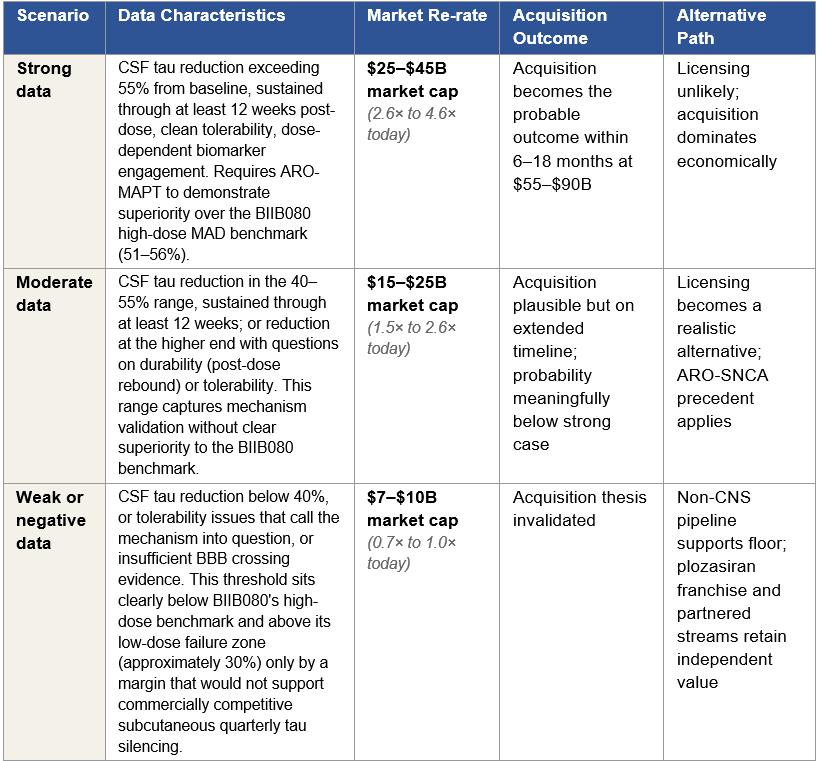

Phase 1 readouts produce continuous measurements on multiple dimensions: CSF tau reduction depth, durability of effect, blood-brain-barrier penetration efficiency, dose-response relationships, and tolerability signals. The market’s response, and the strategic response from potential acquirers, will be calibrated to the specific quality of the data, not to a simple yes/no outcome. This paper therefore organizes its analysis around three scenarios that capture the realistic distribution of Phase 1 outcomes, each with its own re-rate magnitude, acquisition probability profile, and alternative licensing path. The thresholds for each scenario are anchored to the published BIIB080 Phase 1b benchmark, the most directly comparable tau-silencing dataset in the clinical literature. The BIIB080 high-dose cohorts (60 mg monthly, 115 mg quarterly) achieved 51–56% CSF total tau reduction during the 3-month multiple ascending dose treatment period, with sustained approximately 60% reduction across all dose groups through the long-term extension. BIIB080 is delivered intrathecally; ARO-MAPT is delivered subcutaneously. A direct biomarker comparison therefore tests whether Arrowhead’s subcutaneous delivery platform achieves tau-silencing pharmacology comparable to or superior to the intrathecal benchmark.

Figure 1: The Three Phase 1 Scenarios and Their Consequences

Figure 1: Three Phase 1 readout scenarios with corresponding re-rate ranges, acquisition outcomes, and alternative paths. Market cap multiples are anchored to Arrowhead’s approximately $9.8 billion current valuation. Per-share implications and detailed bidder dynamics are developed in later sections.

Two investment consequences follow.

First, the asymmetric entry point is today, before the Phase 1 data arrives. Under the strong data scenario, the re-rate alone produces a 2.6× to 4.6× return, and a subsequent acquisition at the Stage 1 range of $55 to $90 billion extends that to 5.6× to 9.2×. Under the moderate scenario, the re-rate produces a 1.5× to 2.6× return with extended upside optionality. Under the weak scenario, the downside is bounded by the non-CNS business at approximately 70–100% of today’s market cap. The expected value calculation across the distribution is favorable to entering a position today rather than waiting for the readout.

Second, the investor’s task today is not to predict which scenario will materialize, because Phase 1 data quality cannot be forecast with precision. The task is to assess the prior probability of each scenario given what is currently known: BIIB080’s validation of MAPT-silencing as a biomarker-active mechanism in humans, trontinemab’s validation of TfR1-mediated blood-brain-barrier transcytosis as a therapeutic-scale delivery route, Arrowhead’s non-human-primate CSF tau reduction data, and the ARO-MAPT Phase 1 dose escalation design. The weight of this prior evidence reduces the probability of the weak scenario below what the current market cap implies. Section VI quantifies this gap using Monte Carlo simulation across nine input variables; the probabilistic case is built there.

A note on terminology and the longer horizon.

Throughout this paper, “Stage 1” refers to the acquisition outcome that follows from the strong Phase 1 scenario: the $55 to $90 billion range developed in Section II and the sections that follow. “Stage 2” refers to the valuation window that opens if positive Phase 1 data does not produce a transaction within 12 to 18 months and Phase 2 cognitive endpoint data subsequently reads out positive in 2029–2030, which the paper estimates at approximately $110 to $150 billion. Stage 2 is treated as conditional forward optionality rather than a primary scenario; the analysis focuses on the Phase 1 readout and its immediate consequences because that is where the asymmetric investment opportunity lives.

If ARO-MAPT delivers, Arrowhead will either be acquired or will license ARO-MAPT at economics that produce a multi-fold return from today's market cap. If ARO-MAPT does not deliver, the downside is bounded by a real commercial business that exists independent of the platform thesis. The analysis in this paper commits to specific ranges for each path.

II. Price vs. Value

Arrowhead is worth somewhere between $55 billion and $90 billion in a competitive acquisition process if ARO-MAPT’s Phase 1 data meets the strong-case threshold developed in Section I. That range is roughly six to nine times today’s market cap. Both the market cap and the acquisition range are correct numbers. They answer different questions.

Today’s market cap is a price. A price is what the marginal public investor is willing to pay for the marginal share of common stock on any given trading day. It is the aggregate output of rNPV analysis applied by thirteen sell-side analysts, institutional positioning decisions made by portfolio managers who model disclosed programs against stage-dependent probability assumptions, and retail and algorithmic trading that moves on headlines and momentum without reference to the underlying asset’s strategic value. The price fluctuates with market sentiment, sector rotation, and news flow. It is real, and it is the liquidity-weighted consensus of what a diversified portfolio holder should pay for the right to own the share today.

The $55 to $90 billion range is a valuation. A valuation is what a strategic acquirer, evaluating the asset against their own infrastructure, their competitive landscape, and their long-term strategic plan, concludes the asset is worth plugged into their operations. It is the product of detailed synergy analysis, competitive positioning analysis, regulatory and commercial infrastructure analysis, and, critically, the cost-of-not-owning-it calculation that incorporates what happens if a competitor secures the platform first.

These two numbers diverge for Arrowhead specifically because the platform sits at a delivery inflection point and the public market cannot price platform inflections. Understanding why this is structurally true, not a temporary inefficiency that will correct through ordinary trading, is the foundation of the rest of this paper’s argument.

Why Big Pharma Does Not Use rNPV to Value Acquisitions

rNPV is the standard methodology taught in every pharmaceutical finance MBA program and applied by every sell-side analyst covering biotech. Estimate peak revenue for a drug program. Apply stage-dependent success probability. Discount back to present value. Sum across programs.

The methodology is internally consistent, defensible against audit, and appropriate for diversified pipeline companies where programs are largely independent. It is also structurally inadequate for platform companies at delivery inflection points, which is why no pharmaceutical M&A team applies rNPV as the primary valuation framework for acquisition decisions. M&A teams build their own rNPV as a standalone baseline, the number that anchors the floor of what a rational board would accept, and then apply strategic value adjustments, synergy quantification, competitive positioning analysis, and scenario modeling to arrive at the authorized bid range. The rNPV number is not the prediction of acquisition price, it is the floor beneath the acquisition price. The ceiling is set elsewhere.

The Eight Reasons Strategic Value Analysis Produces a Different Number

For Arrowhead specifically, eight structural factors drive the divergence between public market rNPV-derived pricing and strategic acquirer valuation. These are not rhetorical flourishes. Each one represents a specific valuation input that appears in an acquirer’s model and does not appear in a sell-side rNPV.

One: Platform optionality and correlated probability updates.

TRiM has validated delivery across six tissue types, five clinically (liver, lung, muscle, adipose, and CNS neurons via subcutaneous BBB crossing) and one preclinically (ocular). When ARO-MAPT validates subcutaneous TfR1-mediated BBB delivery, the probability of success for ARO-SNCA, ARO-HTT, ARO-ATXN3, and every future CNS program sharing that delivery mechanism rises simultaneously. rNPV treats each program as an independent probability tree. An acquirer treats these probability updates as correlated, which produces materially higher expected portfolio value.

Two: The engine generates candidates faster than rNPV can model them.

Arrowhead’s undisclosed pipeline includes a cardiometabolic program labeled Gene X, presented at the 7th Annual CNS Delivery Summit in December 2025 with approximately 90% mRNA knockdown in non-human-primate brains. That program is not in any sell-side model. An acquirer is not buying the disclosed pipeline; they are buying the engine that generates future pipelines. The engine has economic value independent of any specific current program.

Three: Acquirer-specific synergy.

Lilly’s commercial infrastructure reduces the cost of commercializing ARO-MAPT by approximately 20–25 points of margin. Roche’s trontinemab overlap reduces manufacturing and regulatory costs by 10–15 points. Novartis’s existing ARO-SNCA collaboration reduces technical integration costs by 5–10 points. These synergies are acquirer-specific, meaning they appear in an acquirer’s internal model and are entirely absent from any rNPV. The synergy premium is what allows different bidders to arrive at meaningfully different internal valuations for the same asset, the basis of competitive auction dynamics.

Four: Defensive value.

If Lilly does not acquire Arrowhead and Roche does, the competitive damage to Lilly’s Kisunla franchise has a present value of $15 to $30 billion over a decade. This is not a hypothetical cost. It is a real strategic liability that a rational acquirer factors into willingness to pay. rNPV cannot model competitive scenarios because rNPV is a single-entity cash-flow model. Defensive value is one of the largest single reasons acquirers bid above standalone rNPV.

Five: Combination therapy economics.

A two-mechanism AD franchise, IV amyloid clearance paired with subcutaneous quarterly tau silencing, has pricing power that neither asset achieves standalone. Combination regimens in oncology and immunology command 25–40% premiums over component pricing. For Lilly, the combination of Kisunla and ARO-MAPT is commercially additive in ways that neither drug can replicate individually. For Roche, trontinemab and ARO-MAPT combined produce the only two-mechanism AD franchise in existence where both drugs use TfR1-mediated BBB transcytosis as their delivery route. This scientific and commercial coherence is priced in the acquirer’s model and absent from sell-side rNPV.

Six: Diagnostic-therapeutic franchise coherence (Roche-advantaged).

Roche owns the Elecsys laboratory diagnostic platform, the dominant global infrastructure for Alzheimer’s blood-based biomarker testing. A Roche acquisition of Arrowhead creates a vertically integrated franchise: patient identification with Elecsys pTau-181 and pTau-217 assays, amyloid clearance with trontinemab, tau silencing with ARO-MAPT, and progression monitoring with the same biomarker platform. Note that Roche co-developed the Elecsys pTau blood tests with Lilly under a 2023 partnership, and Elecsys pTau-181 received FDA approval for primary care use in October 2025, so diagnostic access itself is not exclusive to a Roche bid. What remains uniquely Roche’s is ownership of the diagnostic infrastructure, per-test revenue capture across all AD testing volumes, and the ability to vertically integrate diagnostic-therapeutic economics without a partnership revenue-share. That vertical integration is strategic value that appears in Roche’s model and nowhere else.

Seven: Manufacturing and delivery moat.

TRiM requires proprietary chemistry, conjugation, and purification at scale. Arrowhead’s Verona facility provides three operational GMP lines with a 2028 option to acquire 6.24 adjacent acres for commercial-scale expansion. Replacement cost of building this infrastructure from scratch is approximately $2 to $4 billion and five to seven years of construction and qualification. An acquirer values this infrastructure as strategic currency, immediately usable capacity that contract manufacturers cannot replicate. The 6.24-acre adjacent parcel under option through 2028 is an additional layer of strategic value that deserves specific attention. Exercising the option and building expansion capacity on the adjacent parcel would cost an acquirer an estimated 40–60% less than constructing a comparable greenfield GMP facility at a new location, with a timeline compression of roughly 18–24 months. The cost advantage reflects reuse of existing site infrastructure (utilities, permits, environmental qualification, shared services) and partially reusable design work; the time advantage reflects the elimination of site selection, permitting, and initial regulatory qualification phases. For an acquirer planning to scale TRiM manufacturing across multiple commercial products over the next decade, this expansion pathway is not a theoretical asset, it is a pre-positioned capability with quantifiable economic value that a standalone Arrowhead would realize more slowly. rNPV does not assign value to manufacturing beyond the implicit assumption that production capacity exists.

Eight: Accelerated development through acquirer clinical infrastructure.

Lilly and Roche each operate thousands of active clinical trial sites globally, with dedicated CNS trial infrastructure and established protocols for AD-specific enrollment. Plugging ARO-MAPT into that network compresses Phase 2 and Phase 3 enrollment timelines by an estimated 12 to 24 months compared to Arrowhead running these trials standalone. For a Phase 3 AD trial running four to six years, that time compression has material present value; earlier approval, earlier revenue, earlier patent-life capture. This value appears in an acquirer’s model as a line item and is entirely absent from a sell-side rNPV that assumes standalone development timelines.

Why Competitive Bidding Makes Strategic Value Analysis the Only Relevant Framework

In a negotiated M&A transaction with two or more motivated bidders, the final price is controlled by the second-highest bidder’s maximum willingness to pay plus a minimum increment to win. This is not a theoretical proposition; it is the mechanical consequence of auction dynamics applied to corporate M&A. The auction mechanism produces price discovery by forcing each bidder to reveal, through the act of raising their bid, progressively more of their internal valuation.

For Arrowhead post-Phase 1, under the strong data scenario developed in Section I, three strategic bidders, Lilly, Roche, and Novartis, evaluate ARO-MAPT against their own strategic value frameworks. Their internal valuations differ, in absolute terms probably by $20 to $40 billion at Stage 1, because each bidder’s synergy stack, defensive liability, and platform integration value is different. But every one of those internal valuations reflects strategic value analysis with acquirer-specific synergy, defensive value, and positioning economics. None of them reflect sell-side rNPV.

The final price is therefore set by the interaction of these strategic valuations, not by the rNPV framework that generates the public-market stock price. The $9.8 billion market cap is an interesting datapoint, it tells an acquirer what they cannot bid below, because Arrowhead’s board would have fiduciary grounds to reject any bid at a trivial premium over market cap. The market cap does not set the ceiling. The ceiling is set by the most motivated bidder’s strategic value number, constrained downward only by the need to exceed the second-highest bidder’s maximum.

The gap between price ($9.8 billion) and strategic value ($55 to $90 billion at Stage 1) is not a market inefficiency that will close through ordinary trading. It is a framework inefficiency that will close only when a framework-appropriate event, positive Phase 1 data, forces the market to shift from rNPV pricing to strategic value pricing. That shift is the re-rate modeled in Section I’s three scenarios.

What an Acquirer Pays For

A strategic acquirer of Arrowhead at Stage 1 is paying for five distinct categories of value. Understanding these categories helps calibrate why the total exceeds any individual asset’s rNPV.

Assets in the current disclosed pipeline.

Plozasiran franchise across FCS (approved), sHTG (near approval), and the CAPITAN CVOT optionality; ARO-MAPT across AD and the orphan tauopathies (PSP, CBD, FTD-MAPT); obesity pipeline; pulmonary programs including ARO-RAGE; complement programs (ARO-C3, ARO-CFB); Sarepta and Novartis partnership streams. These are the programs a sell-side analyst would find in a model, probability-weighted against published trial timelines.

Platform capacity to generate future programs.

Gene X. Ocular TRiM. Cardiomyocyte TRiM. Programs that exist in Arrowhead’s internal roadmap but are not in sell-side models because they have not been disclosed in sufficient detail to model. An acquirer pays for the engine, not just the current output. The engine has produced ARO-MAPT, ARO-RAGE, ARO-SNCA, Gene X, and numerous other candidates; there is no analytical reason to assume it will stop producing.

Strategic positioning.

The cost of not owning the platform if a competitor owns it instead. For Lilly, this is the Kisunla defensive premium, the value of preventing a subcutaneous tau silencer from pressuring the IV amyloid franchise for a decade. For Roche, this is the trontinemab scientific coherence, the value of being the only company to operate both approved TfR1-delivered drugs. For Novartis, this is the ARO-SNCA collaboration integration, the value of controlling the full platform after already paying for partial access.

Infrastructure.

Verona GMP manufacturing with expansion option; clinical operations including the ARO-MAPT Phase 1 protocol execution; TRiM chemistry expertise accumulated over fifteen years of platform development; regulatory team experience across nine IND filings in multiple therapeutic areas. Replacement cost of building this from scratch is $2 to $4 billion and five to seven years of construction, hiring, and qualification. An acquirer integrates this infrastructure on day one.

Optionality on competitive landscape.

The platform becomes more valuable as competitive alternatives emerge (defensive value rises as competitors threaten Kisunla or other approved AD therapies) and as the platform generates additional validated tissue types (offensive value rises as more therapeutic indications become accessible). A Stage 1 acquirer is buying optionality on both directions of this evolution, a call option on defensive value and a call option on offensive platform expansion.

Comparable Pharmaceutical Acquisitions

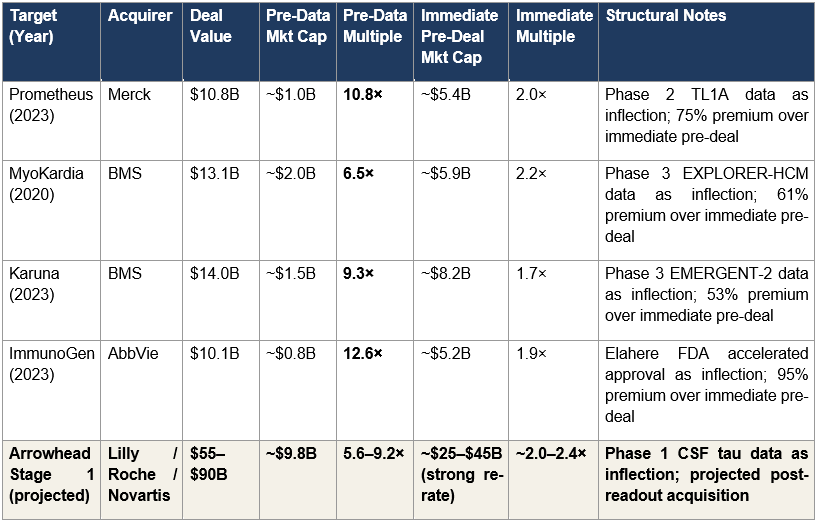

History anchors the math. The question is not whether strategic pharmaceutical acquisitions at multi-billion-dollar premiums over market cap occur, they occur regularly, but at what multiples, for what types of assets, and with what structural characteristics. Figure 2 summarizes four recent comparable transactions, each one a catalyst-driven acquisition involving a clinical-stage or early-commercial biotech with a validated mechanism.

Figure 2: Comparable Pharmaceutical Acquisitions

Figure 2: Four historical pharmaceutical acquisitions with both pre-data and immediate pre-deal multiples. Arrowhead’s projected Stage 1 multiples sit within the historical range on both dimensions: the 5.6–9.2× pre-data multiple is consistent with Prometheus (10.8×), MyoKardia (6.5×), Karuna (9.3×), and ImmunoGen (12.6×); the approximately 2.0–2.4× immediate pre-deal multiple is consistent with the typical acquisition-premium-over-re-rated-market-cap range across all four comparables.

The Prometheus transaction is the most instructive single comparable. Prometheus traded at roughly $1 billion market cap at $36 per share before reporting positive Phase 2 TL1A data in ulcerative colitis (ARTEMIS-UC) and Crohn’s disease (APOLLO-CD) in December 2022. The clinical results triggered a market re-rate to approximately $5.4 billion by April 2023. Merck then paid $10.8 billion (a 75% premium over the re-rated market cap) to acquire the company. The compound multiple from pre-data entry to acquisition close is 10.8×.

The structural parallel to Arrowhead-today is direct. An investor positioned in Prometheus before the Phase 2 data captured the full compound return (10.8×) through the combination of the re-rate and the subsequent acquisition premium. An investor who waited until the data was reported, re-rated the stock, and then bought at the re-rated level captured only the acquisition premium (2.0× from the re-rated market cap). The asymmetric entry point was before the data, not after. Arrowhead today sits in the analogous position: $9.8 billion market cap before Phase 1 data, with a three-scenario outcome distribution that makes today’s entry the asymmetric position.

MyoKardia, Karuna, and ImmunoGen each follow the same structural pattern at somewhat different magnitudes. MyoKardia traded at approximately $2 billion market cap before positive Phase 3 EXPLORER-HCM data; BMS subsequently paid $13.1 billion for a 6.5× pre-data multiple. Karuna traded at approximately $1.5 billion market cap before positive Phase 3 EMERGENT-2 schizophrenia data; BMS subsequently paid $14 billion for a 9.3× pre-data multiple. ImmunoGen traded at approximately $0.8 billion market cap before the November 2022 FDA accelerated approval of Elahere; AbbVie subsequently paid $10.1 billion for a 12.6× pre-data multiple. In each case, the catalyst was a single data or regulatory event that shifted the market’s framework from speculative clinical valuation to acquisition-premium valuation. Arrowhead’s Phase 1 CSF tau readout in 2H2026 is the same category of event.

Note on Alnylam.

Alnylam Pharmaceuticals, Arrowhead’s nearest RNAi competitor, trades at approximately $42 billion as of this writing. Alnylam is not a transaction comparable, it has not been acquired and no public acquisition process is underway, but it establishes what a diversified commercial-stage RNAi platform is worth in the public market today. Alnylam has approved products across multiple indications and validated delivery to liver, muscle, and CNS (via intrathecal administration). Arrowhead, with a more differentiated delivery platform that includes subcutaneous CNS crossing (which Alnylam has not replicated) and a broader clinical pipeline (nineteen programs across ten owned and nine partnered vs. Alnylam’s narrower focus), should not trade at a permanent discount to Alnylam. The current $9.8 billion Arrowhead market cap versus $42 billion Alnylam market cap reflects the delivery-platform validation gap that the Phase 1 readout will resolve. Resolving it in favor of Arrowhead’s subcutaneous CNS validation produces a public market re-rate that begins to close the Alnylam gap, independent of any acquisition process.

Why Large Platform Acquisitions Prove Value-Accretive

The most important historical precedent for understanding why a rational strategic acquirer might pay $55 to $90 billion for Arrowhead is not in the recent comparable-deal data set. It is in Roche’s 2009 acquisition of the remaining public stake in Genentech for approximately $46.8 billion.

At the time of the transaction, the Genentech deal was characterized as expensive, even aggressive. Analysts questioned whether Roche could justify the premium. Within a decade, the acquisition was recognized as one of the most value-accretive transactions in pharmaceutical industry history. The Genentech antibody platform became the foundation of Roche’s oncology franchise and produced multi-hundred-billion-dollar cumulative revenue across Herceptin, Rituxan, Avastin, Perjeta, Kadcyla, and subsequent programs. The apparent premium at acquisition was trivial compared to the value the platform generated under Roche ownership.

The structural argument for an Arrowhead acquisition is the same argument, applied to a different platform technology at a different inflection point. A strategic acquirer who pays $55 to $90 billion for Arrowhead at Stage 1 is not primarily paying for ARO-MAPT in Alzheimer’s disease, though that asset is the immediate value driver. They are paying for a delivery platform that has validated mechanisms across six tissue types and has demonstrated the capacity to generate clinical-stage candidates at a rate that exceeds the industry’s delivery-platform benchmarks. If that platform produces two or three additional approved drugs over the next decade, a reasonable base case given the current pipeline, the acquisition economics justify themselves independent of any single asset’s commercial outcome. The Genentech precedent is the correct analytical frame for understanding what acquirers actually pay for when they acquire platforms, and why the apparent premium at transaction is not the right lens for evaluating the transaction ex post.

Arrowhead’s $9.8 billion market cap reflects public-market rNPV pricing. A strategic acquirer evaluating ARO-MAPT after positive Phase 1 data applies strategic-value analysis, which incorporates synergy, defensive value, and platform optionality that rNPV structurally cannot capture. The gap between those two frameworks is the investment opportunity.

III. Analyst Coverage

Approximately a dozen sell-side analysts cover Arrowhead Pharmaceuticals with active 12-month price targets. The consensus target sits in the range of $76 to $82 per share, implying a target market cap of roughly $10.5 to $11.5 billion. The high-end target on the street is approximately $110 per share, implying a market cap of roughly $15 billion. The low-end target, from a small number of bearish firms, is approximately $35 per share, implying a market cap of roughly $5 billion.

Every one of these numbers is dramatically below the $55 to $90 billion Stage 1 acquisition range developed in this paper. Even the most bullish analyst on the street today is producing a price target that implies a market cap roughly 15% of the Stage 1 acquisition floor. This is not because the analysts believe Arrowhead is worth less than the market assigns; the consensus target represents a modest premium over the current price. It is because the institutional sell-side price target framework cannot accommodate the kind of conditional acquisition thesis this paper describes.

Sell-side price targets are built on three structural constraints that prevent strategic acquisition value from being incorporated.

Twelve-month time horizon.

A sell-side price target is a prediction of what the stock will trade at in approximately twelve months under normal-course-of-business operating assumptions. It is not a target price under an acquisition scenario. An analyst whose 12-month price target reflected an 8× return from current prices would be immediately accused of speculation; their compliance department would flag the note; their sales force would not distribute it. The framework is designed to produce small-magnitude price movements against current prices, which structurally excludes acquisition value by construction.

Probability-weighted scenarios around a base case.

Most sell-side models produce a base case (rNPV-derived), a bull case (somewhat higher peak revenue or earlier timelines), and a bear case (pipeline setbacks). The bull case rarely incorporates acquisition scenarios because acquisitions are idiosyncratic events that cannot be probability-weighted in a defensible way for a 12-month horizon. The analyst who writes “my bull case assumes a $70 billion acquisition from Lilly” is producing an unmodelable claim. The analyst who writes “my bull case assumes 15% higher peak sales and a 12-month earlier launch” is producing a standard, defensible sell-side bull case. The framework selects against the former and selects for the latter.

rNPV as the central valuation discipline.

Every covering analyst uses some variant of rNPV. As established in Section II, this methodology is appropriate for diversified pipeline companies but systematically inadequate for platform companies at delivery inflection points. rNPV applied to Arrowhead today produces the current spread of target prices across the $35 to $110 per share range. The analysts are not wrong within their framework, they are correctly applying an inappropriate framework.

The Implication

When Phase 1 data arrives in the second half of 2026 and the stock re-rates, sell-side coverage will update. Analysts will raise their price targets, probably substantially, given the magnitude of the prior evidence base this paper has laid out, but their updated price targets will still reflect rNPV-based frameworks, now with higher probability inputs for the ARO-MAPT program. The analyst consensus after a strong Phase 1 readout will converge toward a target range consistent with the strong-case market cap developed in Section I’s scenario framework. The sell-side consensus, in other words, will eventually arrive at the re-rated market cap this paper projects, but it will do so by tracking the market’s own pricing, not by anticipating it. Even after this re-rate, the analyst consensus will remain well below the acquisition range. The gap between rNPV-derived targets and strategic acquisition value is not a gap that closes; it is a framework boundary.

An individual investor who waits for sell-side price targets to capture the full acquisition thesis will be waiting indefinitely. The analysts’ framework converges on an rNPV-compliant representation of the re-rated market cap. It does not converge on the acquirer’s willingness to pay, because the analysts’ framework cannot produce that number without violating the institutional constraints that define sell-side coverage.

The One Path Toward a Conditional Analyst Note

There is, however, one path by which a sell-side analyst could begin to close this gap without violating any of the structural constraints described above. A conditional scenario note, framed as follows:

If ARO-MAPT delivers positive Phase 1 human data in 2H2026, we believe strategic acquisition interest from Lilly, Roche, or Novartis could realistically value ARWR in the range of $55 to $90 billion, representing a per-share price of approximately $355 to $581 on a fully diluted basis.

That sentence is compliance-defensible because it is conditional and range-bound. It is analytically honest because the math supports it. It is commercially significant because the first analyst who publishes it will produce the most-read piece of research on this stock in years. The remaining analysts will have to respond, either by engaging with the conditional framework or by explicitly rejecting it. In either case, the market begins pricing the acquisition optionality that it has, to this point, been ignoring.

When that repricing occurs, whether because an analyst publishes the conditional note or because Phase 1 data arrives and forces the reframing, the analytical work that preceded the institutional consensus will have served its purpose. Until then, the reader cannot outsource the acquisition-thesis analytical work to the sell side. The framework constraints that produce the current $76 to $82 average price target are the same framework constraints that will prevent the sell-side from naming the acquisition range until after it is no longer an asymmetric entry point.

The dozen analysts covering Arrowhead produce price targets clustered at $35 to $110 per share, 5 to 15 percent of the Stage 1 acquisition range developed in this paper. The analysts are not wrong within their framework; they are applying an rNPV framework that cannot incorporate acquisition value by construction.

IV. The Non-ARO-MAPT Portfolio

The three-scenario framework developed in Section I depends on understanding what Arrowhead is worth besides ARO-MAPT. In the strong scenario, the non-ARO-MAPT portfolio is what an acquirer gets beyond the Alzheimer’s program; it drives a significant portion of the $55 to $90 billion valuation range. In the weak scenario, the non-ARO-MAPT portfolio is what bounds the downside; it establishes the approximately 70 to 100 percent of today’s market cap floor that the Phase 1 failure case assumes.

This section catalogs those assets. It does not attempt to build comprehensive revenue forecasts or probability-weighted valuations for each program; Sections V and VI take up that work using formal valuation methodology. The purpose here is to establish what is in the portfolio, what stage each program has reached, and what makes each relevant to the acquisition thesis.

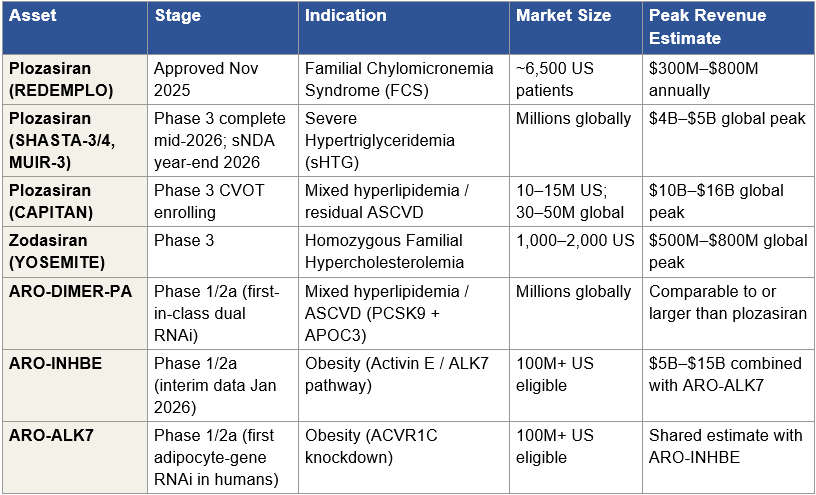

The Commercial Cardiometabolic Franchise

Arrowhead transitioned into a commercial-stage company on November 18, 2025, when the FDA approved REDEMPLO (plozasiran) for familial chylomicronemia syndrome (FCS). REDEMPLO is Arrowhead’s first approved medicine and the anchor of the cardiometabolic franchise. Arrowhead is launching the drug independently in the United States using the One-REDEMPLO pricing model, which establishes a consistent price across current and potential future indications, a deliberate strategic choice that simplifies payor negotiations as the drug expands into additional triglyceride-lowering indications. China’s NMPA approved REDEMPLO for FCS in April 2026, with Sanofi handling commercialization in Greater China under the agreement that Sanofi purchased from Visirna in 2025.

The FCS indication itself is a modest commercial opportunity. Roughly 6,500 people in the United States live with genetic or clinical FCS, characterized by triglyceride levels 10 to 100 times higher than normal and substantial risk of acute pancreatitis. The FCS market, at commercial orphan-disease pricing, represents peak revenue in the range of a few hundred million dollars annually. The commercial importance of REDEMPLO’s FCS approval is not the FCS market itself, it is that the approval establishes plozasiran’s regulatory foundation and commercial infrastructure for the much larger indications that follow.

The severe hypertriglyceridemia (sHTG) opportunity is where plozasiran becomes a major commercial asset. The SHASTA-3, SHASTA-4, and MUIR-3 Phase 3 trials complete in mid-2026, with supplemental NDA filing expected by year-end 2026. The FDA granted Breakthrough Therapy designation for plozasiran in sHTG in December 2025. sHTG is an addressable market measured in millions of patients globally, with peak revenue estimates in the multi-billion-dollar range at commercial pricing. Plozasiran’s head-to-head positioning against Ionis’s Tryngolza in sHTG, where Ionis cut pricing substantially in 2025, is developed in detail in the prior BioBoyScout analysis Redemplo vs. Tryngolza (March 2026). The summary conclusion is that plozasiran’s once-quarterly subcutaneous dosing profile and clinical efficacy support a two-winner market outcome at minimum.

Beyond plozasiran, the cardiometabolic franchise includes zodasiran (Phase 3 for homozygous familial hypercholesterolemia, an orphan indication with commercial optionality) and ARO-DIMER-PA, the first clinical-stage dual-functional RNAi therapeutic. ARO-DIMER-PA silences both PCSK9 and APOC3 genes in a single molecule, with Phase 1/2a dosing of the first subjects initiated January 2026 in mixed hyperlipidemia. Mixed hyperlipidemia is a high-prevalence disorder affecting millions, and the dual-gene approach represents a meaningful platform expansion, not just a new drug candidate but the first demonstration that TRiM can deliver dual-functional RNAi molecules. The commercial opportunity, if Phase 1/2a data supports advancement, is comparable to or larger than plozasiran’s mixed-hyperlipidemia opportunity in CAPITAN.

Figure 3: Non-ARO-MAPT Clinical-Stage Asset Inventory

Figure 3: Clinical-stage assets in Arrowhead’s non-ARO-MAPT portfolio. Commercial infrastructure anchored by REDEMPLO (plozasiran) FCS approval; near-term expansion into sHTG and mixed hyperlipidemia through existing plozasiran trials; standalone obesity program with first human adipocyte-gene knockdown data. Partnered programs (Sarepta, Novartis, Takeda) are discussed separately below. Peak revenue estimates are industry-consensus ranges; probability-weighted rNPV treatment is developed in Section V.

The Obesity Program

Arrowhead disclosed interim Phase 1/2a data from ARO-INHBE and ARO-ALK7 in January 2026. Both programs target the Activin E / ALK7 pathway, a mechanism that is mechanistically distinct from GLP-1 receptor agonism and addresses specific limitations of current obesity standard-of-care: loss of lean mass, GI tolerability, reduced response in patients with diabetes, and disproportional fat mass regain after therapy cessation.

The interim data is clinically meaningful. ARO-INHBE monotherapy produced 9.9 percent visceral fat reduction at week 16 (single dose) and 15.6 percent placebo-adjusted visceral fat reduction at week 24 (two doses), with a 3.6 percent increase in lean muscle tissue. In combination with tirzepatide, ARO-INHBE approximately doubled weight loss and tripled reductions in visceral fat, total fat, and liver fat compared to tirzepatide alone in obese patients with type 2 diabetes. ARO-ALK7 became the first RNAi therapeutic to demonstrate knockdown of an adipocyte-expressed gene in humans, achieving 88 percent mean ALK7 mRNA reduction (94 percent maximum) and 14.1 percent placebo-adjusted visceral fat reduction from a single dose at week 8.

The strategic significance of the obesity program to an acquirer is material. Lilly and Novo Nordisk have built multi-billion-dollar franchises around GLP-1 mechanisms; both face pressure from next-generation approaches that address GLP-1’s limitations. An obesity asset that preserves lean mass, improves GLP-1 combination economics, and addresses the T2D subpopulation where GLP-1s underperform is commercially valuable as standalone or as a combination therapy with existing GLP-1 backbones. Arrowhead has stated its intention to keep both ARO-INHBE and ARO-ALK7 in-house through development, which means an acquirer of Arrowhead inherits both programs intact.

Additional Clinical Programs

Arrowhead’s pulmonary franchise, centered on ARO-RAGE for severe uncontrolled asthma and related indications, continues to advance through Phase 2. The complement franchise (ARO-C3, ARO-CFB) is in earlier stages but covers indications including IgA nephropathy, geographic atrophy in AMD, and paroxysmal nocturnal hemoglobinuria, each with multi-billion-dollar commercial potential in its primary indication. These programs do not carry the same magnitude of near-term catalyst value as plozasiran or the obesity candidates, but they contribute to the platform breadth that acquirers value.

Partnered Programs: Sarepta, Novartis, and Takeda

Arrowhead’s three largest active partnerships represent substantial inherited deal value for any acquirer.

The Sarepta Therapeutics agreement, closed February 2025, covers four clinical-stage programs (ARO-DUX4 for facioscapulohumeral muscular dystrophy, ARO-DM1 for myotonic dystrophy type 1, ARO-MMP7 for idiopathic pulmonary fibrosis, ARO-ATXN2 for spinocerebellar ataxia 2) plus three preclinical programs, with Sarepta able to nominate up to six additional targets during a five-year term. The transaction economics at closing included $500 million upfront, $325 million equity investment at $27.25 per share (a 35 percent premium at the time), $250 million in equal annual installments over five years, and up to $300 million in near-term milestones tied to ARO-DM1 Phase 1/2 enrollment progress. Total deal value, including all future milestones and royalties, is up to approximately $11 billion. Arrowhead also manufactures clinical drug supply for all programs and commercial drug product for the four clinical programs, which represents ongoing revenue-sharing economics that persist through commercial launches.

The Novartis agreement, closed October 2025, grants Novartis exclusive worldwide rights to ARO-SNCA, the alpha-synuclein siRNA for Parkinson’s disease and other synucleinopathies, plus additional collaboration targets. The transaction economics at closing included $200 million up front with up to $2 billion in potential milestone payments plus commercial royalties. The strategic significance of the Novartis deal is compounded by its use of the same subcutaneous CNS-delivery mechanism that underlies ARO-MAPT. Novartis’s commitment to ARO-SNCA at a preclinical stage, based on the delivery platform’s demonstrated non-human-primate data, is external validation of the same delivery mechanism whose translation to humans the Phase 1 ARO-MAPT readout will resolve.

The Takeda agreement on fazirsiran (ARO-AAT) for alpha-1 antitrypsin deficiency-associated liver disease is earlier-established but represents structurally different deal economics from Sarepta and Novartis. The program is actively enrolling in the 160-patient Phase 3 REDWOOD trial, with primary endpoint (≥1 stage reduction in liver fibrosis by biopsy) at week 102. Phase 2 SEQUOIA data showed 94 percent median reduction in hepatic Z-AAT accumulation, 68 percent mean reduction in histologic globule burden, and fibrosis regression in 50 percent of treated patients, results published in The New England Journal of Medicine. Fazirsiran carries FDA Breakthrough Therapy designation for AATD-LD. Deal economics provide Arrowhead with a 50/50 US profit share and tiered 20 to 25 percent royalties on ex-US net sales, a structurally more lucrative economic profile than the pure-royalty partnerships, and one that an acquirer inherits in full.

Beyond Sarepta, Novartis, and Takeda, Arrowhead maintains smaller partnerships and revenue streams from GSK, and Visirna/Sanofi (the latter for Greater China rights to plozasiran). Each contributes milestone and royalty streams; none individually moves the acquisition thesis, but collectively they demonstrate a pattern of institutional pharma validation of the TRiM platform across multiple therapeutic areas.

The Undisclosed Pipeline

Arrowhead presented preclinical data at the 7th Annual CNS Delivery Summit in December 2025 showing approximately 90 percent mRNA knockdown in non-human-primate brains for a deliberately undisclosed cardiometabolic target labeled Gene X. Other undisclosed programs exist across ocular TRiM delivery and cardiomyocyte TRiM delivery, tissue-specific delivery mechanisms that extend the platform’s validated range but have not been assigned to specific clinical candidates publicly.

These undisclosed programs do not appear in any sell-side model. They are the forward output of the platform engine. For an acquirer, they represent pre-disclosed optionality: a pipeline that is already producing at a rate the sell-side cannot model, priced into acquisition valuations because acquirers buy the engine, not just its current disclosed output.

What This Portfolio Establishes

Taken together, the non-ARO-MAPT portfolio establishes two things that the thesis depends on.

First, a non-CNS floor in the weak scenario.

If ARO-MAPT Phase 1 data fails the minimum thresholds developed in Section I, Arrowhead remains a commercial-stage company with an approved first-in-class RNAi therapeutic in plozasiran, near-approval sHTG expansion, a meaningful obesity program with human data, multiple clinical-stage programs in cardiometabolic and pulmonary indications, and ongoing milestone and royalty streams from Sarepta, Novartis, Takeda, and other partnerships. The probability-adjusted value of this business sits near today’s market cap, not dramatically above or below, which is what Section I’s weak scenario asserts.

Second, an acquisition-scenario addition beyond ARO-MAPT.

In the strong Phase 1 scenario, an acquirer is not paying $55 to $90 billion for ARO-MAPT alone. They are paying for ARO-MAPT plus plozasiran’s commercial trajectory, plus the obesity program with best-in-class potential in a mechanism GLP-1 incumbents do not own, plus the inherited Sarepta, Novartis, and Takeda deal economics, plus the platform engine’s undisclosed pipeline output. Each of these is modest individually compared to ARO-MAPT; together they account for a meaningful share of the acquisition range.

Before a single ARO-MAPT scenario is modeled, Arrowhead’s non-CNS portfolio supports a standalone acquisition value of $22 to $34 billion. This is the floor that bounds the weak-scenario downside and the foundation on which the ARO-MAPT acquisition premium is built.

V. Valuation Methodology

Large pharmaceutical acquisitions are valued using four methodologies in parallel, each producing a number that is then triangulated against the others. Understanding how M&A teams actually do this work helps calibrate the $55 to $90 billion Stage 1 acquisition range against defensible methodology rather than asserting it.

Each methodology answers a different question. rNPV asks what the asset is worth on its own cash flows. Peak revenue multiple asks what the market is paying for comparable assets on a revenue basis. Comparable transactions asks what acquirers have paid in similar situations. Monte Carlo asks what the probability distribution of outcomes looks like under realistic input ranges. An acquirer’s M&A team runs all four and looks for convergence. When the four methods converge on a similar range, the thesis is robust. When they diverge, something is off, either the inputs are mis-specified, or the strategic framework is wrong, or both.

Method 1: Risk-Adjusted Net Present Value (rNPV)

rNPV serves as the standalone baseline, the value of the target company operating independently, without acquirer synergies. The M&A team produces their own rNPV using their internal assumptions rather than relying on sell-side consensus, but the framework is similar to sell-side work: estimate peak revenue for each program, apply stage-dependent success probability, discount cash flows at a discount rate appropriate to the asset class, sum across the portfolio.

For Arrowhead, the bottom-up gross sum-of-parts is approximately $83 to $165 billion. Plozasiran franchise across all three indications (FCS approved, sHTG near approval, CAPITAN mixed hyperlipidemia CVOT) contributes approximately $22 to $34 billion on probability-weighted peak revenue. ARO-MAPT in Alzheimer’s disease, at conservative pre-catalyst probability assumptions of 20 to 25 percent at Stage 1, contributes approximately $32 to $54 billion. Orphan tauopathies (PSP, CBD, FTD-MAPT) contribute $8 to $18 billion. Partnered streams (Sarepta, Novartis, Takeda, and smaller agreements) contribute $8 to $18 billion in milestone and royalty-adjusted present value. Extended platform programs, including the obesity franchise, complement, pulmonary, and undisclosed programs, contribute $13 to $41 billion depending on which ones are assigned non-trivial probabilities. The distribution is wide because pipeline probabilities vary materially across assets and discount assumptions compound over long commercial horizons.

After applying a conservative 40 to 50 percent portfolio-level probability haircut, which reflects execution risk across the full asset inventory rather than treating every program’s success as independent, the standalone rNPV range is approximately $45 to $65 billion. An M&A team’s rNPV produces a substantially higher figure than sell-side consensus for three specific reasons. First, M&A teams apply asset-specific probability adjustments after data maturity events rather than industry base rates; sell-side CNS programs are typically assigned 10 to 15 percent probability of approval, while an M&A team looking at ARO-MAPT post-Phase-1 applies 20 to 25 percent because BIIB080 has validated MAPT-silencing mechanism in humans and trontinemab has validated TfR1-mediated BBB delivery. Second, M&A teams include platform optionality, undisclosed pipeline programs, manufacturing capacity, and partnered milestone streams that public-market models typically exclude or heavily discount. Third, M&A teams use discount rates that reflect the acquirer’s weighted cost of capital (8 to 10 percent) rather than the small-cap biotech risk premium sell-side analysts bake into their DCF models (12 to 15 percent). The cumulative effect produces an M&A-internal rNPV two to three times the sell-side consensus for the same underlying asset.

The $9.8 billion current market cap reflects a much deeper delivery-risk discount than even the probability-haircut rNPV supports. The gap between the current market cap and the $45 to $65 billion standalone rNPV range is the first piece of evidence for systematic mispricing. The gap between the $45 to $65 billion standalone rNPV and the $55 to $90 billion Stage 1 acquisition range is the synergy premium, addressed in a later subsection.

Method 2: Peak Revenue Multiple

M&A teams cross-check rNPV using peak revenue multiples drawn from comparable pharmaceutical transactions. Historical pharmaceutical acquisitions have transacted at 4 to 7 times peak revenue for validated-mechanism single-asset deals and 2 to 4 times peak revenue for diversified pipeline companies. The mechanism of this methodology is different from rNPV: it captures what acquirers have paid for the right to commercialize assets at scale, which implicitly includes both standalone cash flow value and some of the strategic premium that pure cash-flow discounting misses.

Arrowhead’s risk-adjusted peak revenue at Stage 1 is approximately $18 to $25 billion. Plozasiran franchise contributes $8 to $12 billion (FCS at a few hundred million, sHTG at $4 to $5 billion global peak, CAPITAN mixed hyperlipidemia at $3 to $7 billion risk-adjusted). ARO-MAPT across AD and orphan tauopathies contributes $10 to $13 billion at the 20 to 25 percent probability used in rNPV (which produces $8 to $10 billion from AD alone at peak) plus tauopathies at smaller but non-trivial contribution. Minor contributions from obesity, partnered streams, and other programs round out the estimate.

Applied to a 4 to 6 times multiple, the validated-mechanism range, appropriate for a company where the core assets are either approved, near-approved, or about to resolve a binary catalyst, this produces an enterprise value range of approximately $72 to $120 billion. The peak revenue multiple range runs higher than rNPV because it implicitly captures a portion of the strategic premium that rNPV excludes by construction. This is not a methodology error; it is a different question being answered. rNPV asks “what are the risk-adjusted cash flows?” Peak revenue multiple asks “what has the market paid for comparable revenue streams?” The two numbers should differ, and they do.

Method 3: Comparable Transaction Multiples

The comparable transaction framework anchors against market-cap multiples from closed pharmaceutical acquisitions. As developed in detail in Section II (Figure 2), validated-mechanism platform acquisitions have transacted at pre-data multiples of 6.5 to 12.6 times pre-data market cap in the four closest comparables: Prometheus 10.8×, MyoKardia 6.5×, Karuna 9.3×, ImmunoGen 12.6×. Each of these deals involved a catalyst-driven acquisition where a pharmaceutical acquirer paid a compound multiple that captured both the post-catalyst market re-rate and the acquisition premium.

Applied to Arrowhead’s current $9.8 billion market cap at a Stage 1 multiple range of 5.6 to 9.2 times, the comparable transactions methodology produces $55 to $90 billion in enterprise value. This range sits below the average historical multiple (which would produce approximately $95 billion at the midpoint) for two reasons. First, the restructured paper takes a conservative position on Stage 1 relative to the comparable set; the comparables average 9.8× pre-data multiple, while the paper uses 5.6 to 9.2× to reflect execution uncertainty and to leave room for Stage 2 and beyond. Second, Arrowhead’s pipeline breadth is greater than any single comparable, which moderates the per-asset multiple that would otherwise apply to a single-asset comparable.

The comparable transactions methodology is the most directly anchored of the four methods because it references actual deal consideration rather than modeled cash flows. An M&A team defending a $55 to $90 billion bid to a board uses the comparable transactions work first because it is the least theoretically contestable: the deals happened, the multiples are what they are, and the analytical question becomes whether Arrowhead’s structural characteristics justify placing the deal within, above, or below the comparable range. The paper’s position is that Arrowhead’s characteristics justify a placement within the range, anchored to the Stage 1 pre-data multiple.

Method 4: Monte Carlo Simulation

The fourth methodology is probabilistic rather than deterministic. Rather than produce a single enterprise value, Monte Carlo simulation runs 10,000 iterations varying key input assumptions across their stage-appropriate distributions: ARO-MAPT AD approval probability, peak revenue, discount rate, regulatory timing, pricing dynamics, competitive entry, platform success across non-disclosed programs. The output is a probability distribution of enterprise value outcomes, from which the M&A team identifies the range that defines a value-accretive bid.

Section VI develops the Monte Carlo in detail, including the input distributions and the resulting enterprise value percentiles. The summary at this level: the Monte Carlo median enterprise value at Stage 1 sits in the range of $75 to $105 billion, with the 25th to 75th percentile band spanning approximately $55 to $140 billion. The median range sits above the rNPV band and below the upper end of the peak revenue multiple band, which is the expected pattern when rNPV is conservative on probability inputs and peak revenue multiples capture partial strategic premium.

The Synergy Adjustment

The four standalone methodologies produce a distribution of standalone enterprise values, what the target is worth without reference to the specific acquirer. In any real M&A transaction, however, the final price reflects acquirer-specific synergies: the additional value that an asset generates when plugged into a particular acquirer’s infrastructure rather than operating standalone. This synergy premium is the difference between the standalone valuation and the acquisition price.

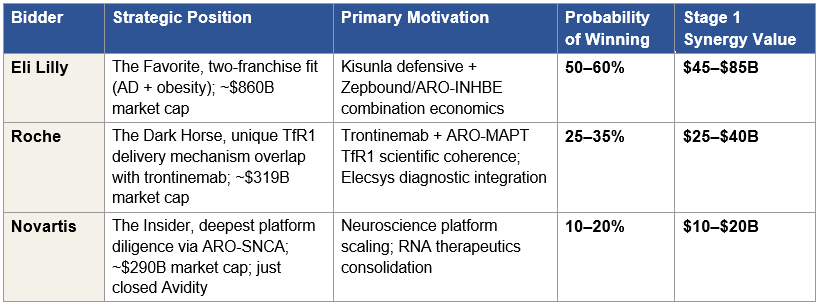

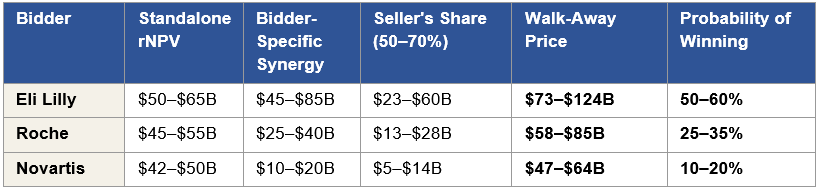

Stage 1 synergy values are acquirer-specific and substantial. For Lilly, the total synergy has two components. The first, AD-focused synergy, comprising Kisunla defensive value, the Kisunla + ARO-MAPT two-mechanism AD franchise pricing power, and commercial infrastructure integration, produces an estimated $30 to $50 billion. The second, obesity-focused synergy, comprising defensive value against competitor acquisition of Arrowhead’s obesity program, the tirzepatide + ARO-INHBE combination product economics (where January 2026 Phase 1/2a data showed doubled weight loss and tripled visceral/total/liver fat reductions versus tirzepatide alone), and commercial synergy across Lilly’s obesity auto-injector platform, produces an estimated $15 to $35 billion. Combined, Lilly’s Stage 1 synergy value is approximately $45 to $85 billion. For Roche, the trontinemab scientific coherence, the Elecsys diagnostic-therapeutic integration, and the Genentech antibody platform integration produce approximately $25 to $40 billion. For Novartis, the ARO-SNCA collaboration scaling and broader CNS expertise integration produces approximately $10 to $20 billion. Section X develops these synergy values in detail and defends the specific numbers against counter-arguments, including why Lilly’s two-franchise strategic fit produces a total synergy materially larger than the other bidders’.

In any negotiated acquisition, buyers capture 50 to 70 percent of synergy value for their own shareholders and pay 30 to 50 percent to sellers as the acquisition premium above standalone. Applied to the standalone valuation range and the synergy value range, the math produces the $55 to $90 billion Stage 1 acquisition range: a standalone valuation anchored around the $45 to $65 billion rNPV baseline, plus the seller’s captured share of acquirer-specific synergies, plus the competitive dynamic that drives bidders toward their maximum willingness to pay in an auction process.

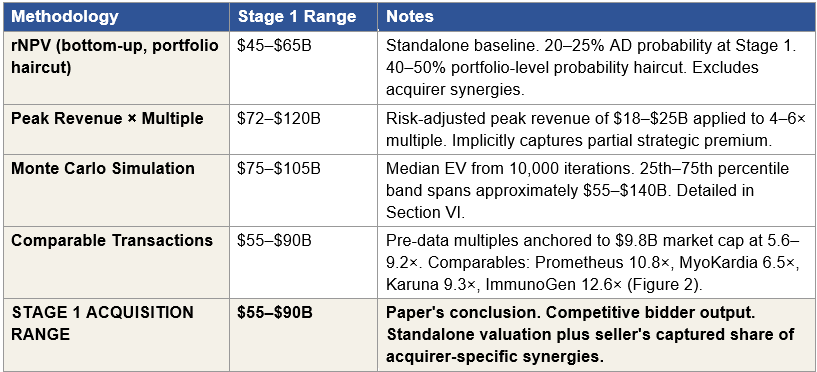

Methodology Convergence

The four standalone methodologies and the synergy adjustment converge on the $55 to $90 billion Stage 1 range. Figure 4 consolidates the output of each methodology at Stage 1.

Figure 4: Methodology Convergence at Stage 1

Figure 4: Four independent valuation methodologies applied at Stage 1, with the paper’s acquisition range for comparison. Each methodology uses independent inputs and assumptions. All four methodology ranges overlap the $55 to $90 billion Stage 1 conclusion: comparable transactions produces the range directly, peak revenue multiple fully contains it, Monte Carlo median sits in the upper band, and rNPV sits just below (reflecting the synergy premium excluded from standalone valuation).

The ranges produced by the four methodologies are not identical, nor should they be. Each methodology answers a different question and captures a different aspect of strategic value. What matters analytically is that all four methodology ranges overlap the $55 to $90 billion acquisition range, meaning every methodology individually produces outputs consistent with the paper’s conclusion. Two of the four (peak revenue and comparable transactions) fully contain the range. Monte Carlo’s median sits inside the upper band. rNPV sits just below, and the gap between rNPV and the acquisition range is the synergy premium that standalone valuation methodologies cannot capture by construction.

When four independent methodologies with different inputs and different theoretical bases produce ranges that converge on the same conclusion, the conclusion is robust. That convergence is the analytical signal that the $55 to $90 billion Stage 1 range is not the output of a single methodology’s assumptions but the consensus of the valuation framework pharmaceutical M&A teams actually use. It is the number an acquirer’s board would see if their team performed this work independently, which is a different claim than saying the market will arrive at this number through ordinary trading.

Four independent methodologies, rNPV plus synergy, peak revenue multiple, Monte Carlo, and comparable transactions, converge at a Stage 1 acquisition range of $55 to $90 billion under the strong Phase 1 scenario. Convergence from methodologies with no shared inputs is the strongest possible analytical signal that the range is structurally correct, not the output of any single model’s assumptions.

VI. Monte Carlo Distribution

The Monte Carlo simulation is the probabilistic counterpart to the deterministic methodologies in Section V. Rather than produce a single point-estimate enterprise value, it runs 10,000 iterations varying nine key input variables across stage-appropriate probability distributions, and reports the resulting enterprise value distribution by percentile. The exercise does two things that deterministic methods cannot. First, it quantifies the uncertainty around each of the four standalone methodology outputs, making clear which assumptions drive the largest swings in enterprise value. Second, it produces a probability-weighted answer to the question any acquirer’s M&A team has to answer for their board: what is the likelihood that a bid at a given price is value-accretive for the acquirer?

The Monte Carlo at pre-Phase-1 produces enterprise value ranges that are dramatically wider than the stage-conditioned ranges that follow each data resolution event. This is the central observation: at today’s information state, the uncertainty around Arrowhead’s fair value is enormous, because the single most consequential variable, ARO-MAPT’s probability of ultimate AD approval, has a pre-Phase-1 distribution that spans an order of magnitude of possible values. Phase 1 data collapses this distribution significantly, which is why the Phase 1 readout is the single largest re-rating event in the Arrowhead timeline.

The Driving Variable: ARO-MAPT AD Approval Probability

The single most consequential input in the Monte Carlo is ARO-MAPT’s probability of ultimate AD approval. This variable is scenario-conditioned: its distribution depends on the information state, which in the restructured framework depends on which of the three Phase 1 scenarios materializes.

At pre-Phase-1 (today’s information state), historical base rates for Phase 1 CNS programs produce a 10 to 15 percent probability of ultimate approval. For ARO-MAPT specifically, the argument for a higher probability rests on BIIB080 having validated MAPT-silencing mechanism in humans and trontinemab having validated TfR1-mediated blood-brain-barrier crossing in humans. These are real but partial validations. An appropriate pre-Phase-1 probability is 15 to 20 percent.

Under the strong Phase 1 scenario, delivery risk is retired by positive human CSF tau reduction data meeting or exceeding the BIIB080 benchmark, the probability that ARO-MAPT will silence MAPT in the human brain is no longer speculative. What remains uncertain is whether tau silencing translates to clinical benefit in a cognitive endpoint trial. The strong-scenario probability of ultimate approval is 20 to 25 percent. This reflects the real residual risk that tau knockdown, even at high magnitude, may not produce the cognitive benefit required for approval, a risk that BIIB080’s CELIA Phase 2 cognitive data will partially but not fully retire.

Under the moderate Phase 1 scenario, CSF tau reduction in the 40 to 55 percent range, mechanism validated without clear superiority to the BIIB080 benchmark, delivery is partially validated but the strength of efficacy signal is weaker. The moderate-scenario probability of ultimate approval is 12 to 18 percent, reflecting retained mechanism viability but compressed superiority assumptions.

Under the weak Phase 1 scenario, CSF tau reduction below 40 percent, tolerability issues, or insufficient BBB crossing evidence, the CNS platform thesis compresses materially. The weak-scenario probability of ultimate approval is 5 to 10 percent. At this level, AD expected value becomes a small contributor to total enterprise value, and the Monte Carlo distribution collapses toward the non-CNS floor.

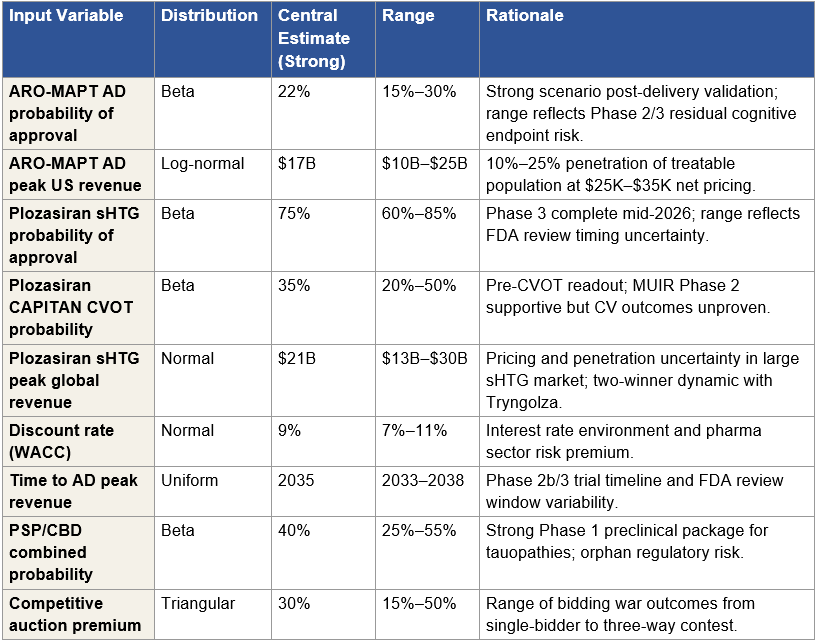

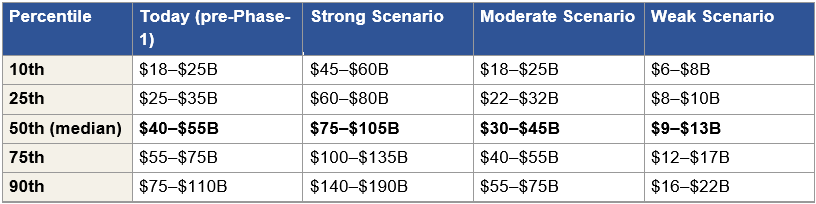

Figure 5: Monte Carlo Input Variables and Distributions

Figure 5: Nine input variables modeled in the Monte Carlo simulation. Central estimates and ranges correspond to the strong Phase 1 scenario. The probability of AD approval and peak AD revenue are the two highest-variance inputs and together drive approximately 60 percent of the distribution width. Moderate- and weak-scenario simulations use the same variable set with scenario-appropriate probability distributions (e.g., AD probability central estimate shifts to 15 percent for moderate, 7 percent for weak).

AD Probability Sensitivity: The Dominant Driver

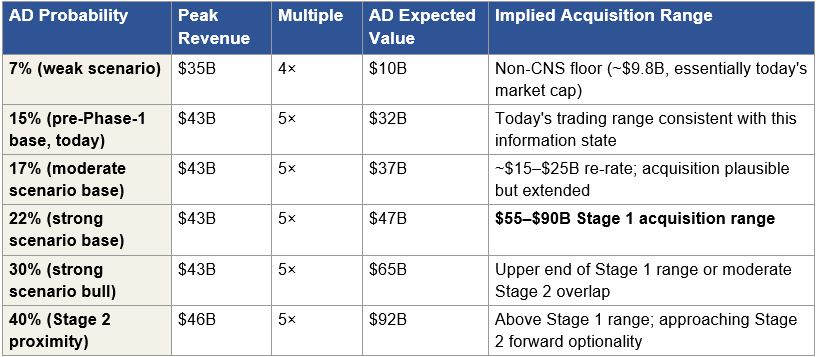

Before examining the full nine-variable Monte Carlo output, it is useful to see the impact of the single most important variable in isolation. Figure 6 shows the AD indication expected value at different probability assumptions, holding peak revenue and multiple at their central estimates.

Figure 6: Sensitivity of AD Expected Value to Probability Assumption

Figure 6: AD indication expected value as a function of probability assumption. The AD indication valuation is dominated by the probability assumption. Each row is internally coherent and represents a different information state. The 22 percent probability at Stage 1 reflects delivery risk retirement without cognitive endpoint confirmation. Individual investors who disagree with this assumption can substitute their own number and recalculate the acquisition range using this sensitivity table. The dominance of this single variable in the distribution motivates running a full Monte Carlo rather than relying on point estimates.

Scenario-Conditioned Enterprise Value Distribution

Figure 7 presents the full Monte Carlo output: enterprise value distribution percentiles under four information states, today (pre-Phase-1), and the three Phase 1 scenario outcomes. Each distribution is based on 10,000 simulations varying all nine input variables within their scenario-appropriate probability distributions.

Figure 7: Scenario-Conditioned Monte Carlo Enterprise Value Distribution

Figure 7: Monte Carlo enterprise value distribution by percentile, under four information states. Each distribution reflects 10,000 simulations with scenario-appropriate probability inputs. The median row, bolded, is the central output for each scenario. The distribution is right-skewed pre-Phase-1 because AD probability uncertainty is right-skewed; post-Phase-1 distributions are progressively less skewed as delivery and efficacy risk are retired. The acquisition price in any scenario falls below the enterprise value median, reflecting the competitive discount an acquirer captures by pricing below their maximum willingness to pay.

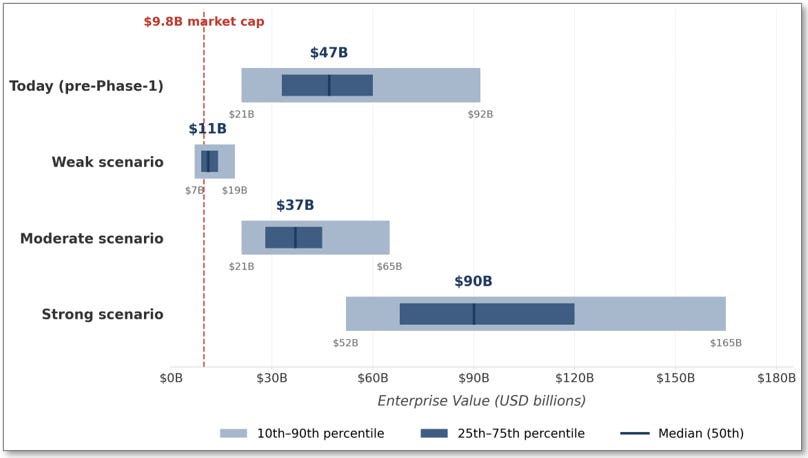

Figure 8: Enterprise Value Distribution by Scenario — Visual Comparison

Figure 8: Monte Carlo enterprise value distribution visualized across four information states. The visual makes two observations immediately legible: first, Arrowhead trades today at approximately the 7th percentile of its own pre-Phase-1 distribution, far below the $47 billion pre-Phase-1 median; second, the jump from today’s median to the Strong scenario median is approximately 1.9×, the single largest repricing event in the Arrowhead timeline. The Weak scenario distribution is bounded near today’s market cap (the non-CNS floor), while the Moderate scenario median sits modestly below the pre-Phase-1 median and the Strong scenario median extends substantially above it.

Key Observations from the Distributions

Today’s market cap prices Arrowhead at roughly the 7th percentile of the pre-Phase-1 distribution.

The pre-Phase-1 Monte Carlo median is $40 to $55 billion, while Arrowhead trades at a $9.8 billion market cap. That valuation corresponds to approximately the outcome in which ARO-MAPT fails entirely and platform optionality evaporates, the scenario the prior evidence base developed in Section I argues against.

The Strong scenario median contains the $55 to $90 billion Stage 1 acquisition range.

The Strong scenario 50th percentile is $75 to $105 billion; the 25th percentile is $60 to $80 billion. The $55 to $90 billion Stage 1 acquisition range sits approximately at the 25th to 40th percentile of the Strong scenario distribution. This placement is the signature of a value-accretive acquisition: the buyer pays below the enterprise value median, which means the acquisition is value-accretive for the buyer in the majority of simulated outcomes. An acquisition priced at the median would require the seller to capture 100 percent of synergy, which does not happen in competitive auctions. The $55 to $90 billion range is where a rational acquirer’s board approves the bid because the probability of overpayment is bounded below 40 percent of the simulated distribution.

The Phase 1 readout is the single largest repricing event.

The jump from today’s $40 to $55 billion pre-Phase-1 median to the Strong scenario’s $75 to $105 billion median is approximately 1.8× to 1.9×. This is the single largest percentile-level re-rating in the Arrowhead timeline, larger than any subsequent data event would produce. The reason: Phase 1 retires the delivery risk that dominates the pre-Phase-1 uncertainty. After Phase 1, the remaining distribution is dominated by cognitive-endpoint uncertainty, pricing, and timing; all important, but none as consequential as the binary question of whether TfR1-mediated subcutaneous delivery produces meaningful tau silencing in humans.

The Moderate scenario still produces a meaningful re-rate.

The Moderate scenario median of $30 to $45 billion represents roughly a 3× to 4.5× lift from today’s $9.8 billion market cap. Even in the scenario where ARO-MAPT produces partial efficacy without superiority to the BIIB080 benchmark, the expected value math supports a meaningful positive return from today’s entry point. The Moderate scenario is not a failure, it is a reduced but still economically positive outcome.

The Weak scenario is bounded.

The Weak scenario median of $9 to $13 billion sits at or slightly above today’s $9.8 billion market cap. The 25th percentile is $8 to $10 billion; the 10th percentile is $6 to $8 billion. Even in the failure case, the distribution is bounded above today’s level at its median and does not collapse into single-digit-billion territory at the 25th percentile. This is the non-CNS floor that Section IV established, expressed in probabilistic terms: the commercial business anchored by plozasiran’s cardiometabolic franchise, the obesity program, and the partnered streams supports a floor valuation that approximately brackets today’s market cap.

Monte Carlo as Confirmation

The Monte Carlo output confirms the three other methodologies from Section V. rNPV ($45 to $65 billion standalone) sits below the Strong scenario Monte Carlo median ($75 to $105 billion), with the gap representing the synergy premium that standalone valuation excludes by construction. Peak revenue multiple ($72 to $120 billion) overlaps the Strong scenario 50th to 75th percentile band. Comparable transactions ($55 to $90 billion) aligns with the Strong scenario 25th to 40th percentile band, which is precisely the band where value-accretive acquisition pricing occurs. The four methodologies converge because the underlying analytical framework they share, probability-weighted asset valuation, strategic premium, competitive bidder dynamics, produces consistent outputs regardless of which methodology is used to generate the point estimate.

What the Monte Carlo adds beyond the deterministic methods is the probability context. An acquirer’s M&A team uses the Monte Carlo to answer the question the board asks: what is the probability that our bid is value-accretive? For a bid at $55 billion, the probability of overpayment against the Strong scenario distribution is approximately 10 to 15 percent, the bid sits near the 15th percentile. For a bid at $90 billion, the probability of overpayment is approximately 35 to 45 percent, the bid sits near the 40th percentile. The range between these two bounds is the $55 to $90 billion Stage 1 acquisition range, and the probability of overpayment across the range is bounded below 50 percent under every simulated input combination. That is the analytical condition that makes the bid approvable at an acquirer’s board. It is also the analytical condition that does not hold at Arrowhead’s current $9.8 billion market cap, a point where the probability of overpayment is essentially zero but the probability of underpayment exceeds 90 percent.

The pre-Phase-1 Monte Carlo median is $40 to $55 billion. Arrowhead trades at $9.8 billion, approximately the 7th percentile of the simulation output. The market is pricing Arrowhead today as if the weak scenario, the outcome in which ARO-MAPT fails entirely, were the probability-weighted base case.

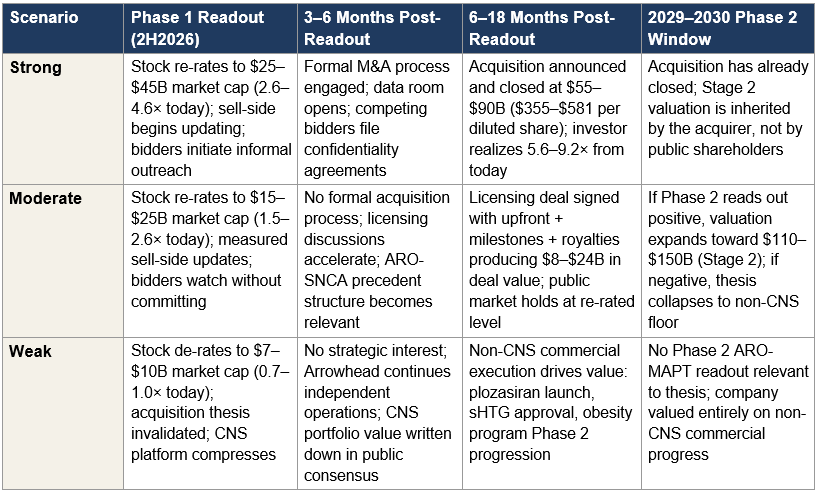

VII. The Three Scenarios

Section I introduced the three Phase 1 readout scenarios as a framework for pricing the investment today. Sections IV through VI built the valuation machinery that each scenario implies. This section narrates what each scenario actually looks like in practice: how the data reads out, how the market reacts, what strategic response each scenario produces from potential bidders and from Arrowhead management, and where the investor ends up across each path through 2030.