The Forced Move, by the Numbers

A numbers guide to why Novartis, Lilly, and Roche may each be cornered into buying Arrowhead, how high each could rationally bid, and where the thesis could break

Robert Toczycki, JD, MBA

bioboyscout.com

bioboyscout@gmail.com

847.227.7909

X: @BioBoyScout

This note translates the game theory trilogy into plain numbers. The Forced Move series argues that three large drugmakers, Novartis, Lilly, and Roche, may each be pushed toward acquiring Arrowhead, not because they want to, but because the cost of letting a rival buy it first can be worse than the cost of buying it themselves. That is what a forced move means in chess: a move you make because every alternative is worse. This note shows how that idea looks once you attach real numbers to it, and how those numbers are built.

A quick word on the patent cliff

Every large drugmaker lives in fear of the patent cliff. A drug is protected by patents for a set number of years. When that protection ends, cheaper copies, generics for ordinary pills and biosimilars for the more complex biologic drugs, flood in, and the original medicine can lose most of its sales within a year or two. A company with a big drug going off patent has a revenue hole to fill, and filling it is urgent.

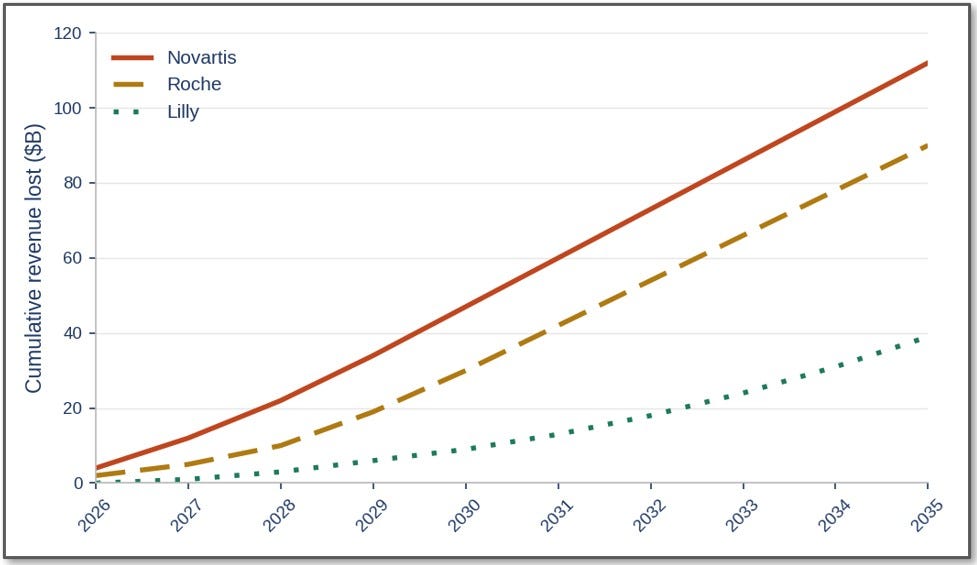

The three companies in this story face that cliff on very different clocks. Figure 1 shows the cumulative sales each one is set to lose to expiring patents over the next ten years.

Figure 1: The patent cliff arrives on three different clocks

Cumulative branded revenue each company is projected to lose to patent expiry, 2026 through 2035. Modeled from public sales and known expiry dates.

Novartis is bleeding now. Its heart-failure blockbuster Entresto, which sold roughly $7.7 billion in 2024, began losing United States protection in 2025, and the company has called 2026 its largest patent-expiry year ever. Roche faces a slower wave that builds mid-decade, led by its multiple-sclerosis drug Ocrevus losing protection around 2028 and 2029. Lilly barely bends, because its giant obesity and diabetes franchise, Mounjaro and Zepbound, is protected into the late 2030s, so its near-term hole is small.

The shape of those three lines is the first half of the story. Novartis needs a replacement engine today. Roche needs one soon. Lilly can afford to wait.

The one idea that changes everything

Arrowhead is attractive to all three because its platform works like a factory for new medicines, which is exactly what a company with a revenue hole needs. That much is ordinary. The idea that turns this into a forced move is less obvious, and it is the heart of the argument.

Most people weigh an acquisition as buy versus do not buy, where not buying simply saves the purchase price. That framing is wrong here. The real choice is buy it yourself versus let a rival buy it. Letting a rival win is not free. You still face your own patent cliff with no new engine to fill it, and now a competitor owns a platform it can turn against your business. Inaction carries a price tag, and once you see that, the math tips.

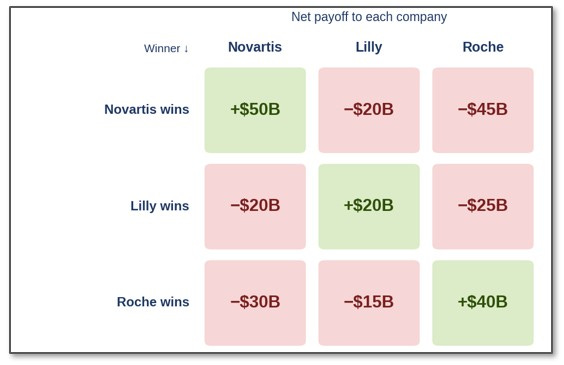

The payoff grid

Figure 2 puts that logic onto a single grid.

Figure 2: The three-way payoff grid

Net present value to each company (columns) under each possible winner (rows), in billions of dollars, at an assumed $120 billion acquisition price. Green is a gain from winning; red is a loss when a rival wins. Modeled base case.

Each row is one possible outcome, the company that wins Arrowhead. Each column is the result for one company. Every square then answers a single question: if the company on the left wins, what happens to the company named at the top?

The green squares run down the diagonal, where a company wins the auction itself, and those are gains. Every red square is an outcome where a rival wins instead, and those are losses. Here is the punchline. Pick any single column and read down it. You will find one green square and two red ones. No company has a comfortable do-nothing option, because if it stays out, one of the other two wins and it takes a loss. The only good outcome is the one you have to pay for. That is the forced move.

A few specifics are worth seeing. Novartis has the most to gain by winning, because its cliff is the most urgent. Roche faces the steepest single loss on the board, the $45 billion it would suffer if Novartis wins, because Arrowhead’s brain-delivery work sits right next to Roche’s own brain franchise, so a Novartis-owned Arrowhead would be a direct threat. Lilly’s squares are the smallest in both directions, because it is the least cornered.

Where the numbers come from

None of these figures are facts pulled from a filing. They are estimates, built from a few simple rules, and it is worth knowing exactly how, so you can judge them for yourself.

Start with the price. The base grid assumes a sale clears at about $120 billion, which sits in the middle of a realistic range for an asset like this.

Next comes the value of owning Arrowhead, which differs by buyer. It starts from a common baseline, the standalone worth of the platform and pipeline, built from the parts in the next section at about $90 billion, then adds an amount unique to each buyer for the synergies and cliff-filling it gains. Subtract the price from that total, and the result is the green diagonal number, the net gain of winning.

Then come the losses, and here a tempting mistake was avoided. It is natural to think a company that loses Arrowhead loses two things: the cliff-filling it misses and the competitive damage of a rival holding the platform. Counting both is wrong. Your patent cliff is unfilled whether Arrowhead stays independent or a rival buys it, so you never actually had that cliff-filling to lose; it belongs entirely to the gain from winning. The only genuine loss from a rival winning is the extra competitive damage that rival does with the platform, over and above the competition an independent Arrowhead already poses, so that is the single thing the red squares count. This keeps the same pipeline from being counted twice, once as a gain and once again as a loss.

What the platform is worth on its own

That $90 billion baseline is not a number borrowed from thin air, and it is worth building from the parts. Figure 3 does that.

Figure 3: Building the $90 billion standalone value

A modeled sum of the parts. The tangible floor rests on named programs and signed contracts; the platform option value is the contested estimate. Risk-adjusted and illustrative.

The tangible floor comes first. Arrowhead’s wholly-owned pipeline, led by the approved triglyceride-lowering drug plozasiran and its much larger late-stage program, alongside the obesity, tau, and complement candidates, carries the most identifiable value, on the order of $43 billion on a risk-adjusted basis. Its partnership streams, the milestones and royalties owed by Sarepta, Amgen, GSK, Novartis, and others, together with net cash, add roughly $12 billion. Those pieces give a tangible floor near $55 billion, the part grounded in named assets and signed contracts.

The platform option value is the rest, about $35 billion, and it is the real bet. This is the worth of the delivery engine itself, its proven ability to reach the liver, lung, muscle, fat, kidney, and now the brain, and to keep generating new programs not yet named. It is the hardest piece to pin down and the easiest to argue over, which is why Figure 3 shows it separately. Value the engine conservatively and the standalone value sits near $90 billion; value it the way a true believer in the platform would, and it climbs well past that.

Two things follow. The $90 billion baseline used throughout this note is a deliberately conservative reading, a solid tangible floor plus a restrained platform value, sitting at the low end of the wider sale range. The single largest source of disagreement about what Arrowhead is worth is therefore not the pipeline, which is fairly concrete, but how much credit to give the engine that keeps building it.

What the precedents say

Modeled numbers feel less abstract when set against real deals, and three precedents are worth knowing. In 2019, Novartis bought The Medicines Company for $9.7 billion, a premium of about 41 percent over the prior month’s average price, to acquire a single siRNA drug, inclisiran, which became its cholesterol medicine Leqvio. That deal put nearly $10 billion behind one asset, from the very company at the center of this analysis. Arrowhead is not one asset; it is a platform with roughly a dozen programs across the body, including the brain.

Two larger deals fill in the picture. In 2021, Novo Nordisk paid $3.3 billion for Dicerna, another RNAi company. In 2023, Pfizer paid $43 billion for Seagen to own an antibody-drug-conjugate platform, financing most of it with about $31 billion of new debt. Large platform deals happen, they clear regulators, and acquirers take on serious debt to do them.

Two lessons carry over. Biotech takeovers routinely price at premiums of 40 percent to 100 percent or more over the trading price, so a wide gap between Arrowhead’s roughly $12 billion market value and a strategic price is the norm, not a stretch. A buyer with an urgent need also pays up, as Novartis did with a double-digit premium for one cardiovascular siRNA when it wanted to anchor that franchise. The platform logic that justified $9.7 billion for inclisiran applies with far more force to an entire delivery engine.

How high would each company bid?

There is a clean way to put a floor and a ceiling on what each company should rationally pay, with the real bid landing somewhere between the two.

The floor is the denial value, the competitive damage a company avoids purely by keeping the most threatening rival from winning. A company should be willing to commit at least this much for defense alone, before counting a single dollar of owning the asset, because preventing that particular rival is worth exactly that avoided loss. For Novartis, letting Roche win would cost about $30 billion, so $30 billion is its floor. For Roche, letting Novartis win would cost about $45 billion, the steepest figure on the board, because a Novartis-owned Arrowhead would aim the brain-delivery platform straight at Roche. For Lilly, letting Novartis win would cost about $20 billion.

The ceiling sits far higher. The most a company should pay is that same denial value plus the full value of owning Arrowhead in its own hands. That works out to roughly $200 billion for Novartis, $205 billion for Roche, and $160 billion for Lilly. Every one of those ceilings towers over any realistic clearing price, which is precisely why a contested auction would run hot.

Put plainly: the floor is the loss avoided, the ceiling is that loss avoided plus the gain from owning, and the rational bid lives in the band between them, pushed upward by how hard the other two press. Folding the gain into the floor would be a mistake, because it would collapse the floor and the ceiling into one number and erase the band entirely.

One subtlety is worth getting right: the ceiling has two layers. The bottom layer is the plain value of owning Arrowhead, and it holds whether or not anyone else bids, because even an independent Arrowhead competes with these three in lipids, in metabolic disease, and in complement, and could partner with any of their rivals at any time. Owning it neutralizes that competitor either way, so part of the ceiling has nothing to do with a bidding war.

The top layer is the rival-control premium, the $30 billion for Novartis or the $45 billion for Roche, the extra harm of a specific, deep-pocketed rival seizing the platform and aiming it at you. That premium exists only while a live rival is actually bidding, and it falls away the moment the rival steps back. The forced move is sharpest in that top layer, yet the layer beneath still gives each company a standing reason to want Arrowhead off the board.

Notice that Roche carries both the highest floor and the highest ceiling, even though its patent cliff is less urgent than Novartis’s. What drives Roche is not its own revenue hole but the prospect of a rival seizing the brain platform, which makes its case a matter of defense rather than need.

Arrowhead’s walk-away: the $90 billion floor

Every walk-away price so far has belonged to a buyer. Arrowhead has one of its own, and it anchors the entire deal. A seller’s walk-away is the value of its best alternative to selling, which for Arrowhead is simply continuing to operate independently. That value is the standalone worth built in Figure 3, about $90 billion. It is the price below which Arrowhead should refuse any offer and stay independent, because below it shareholders are better off keeping the company than selling it. That single number is the floor under everything.

This floor is not a negotiating pose; it has real force. A public-company board owes its shareholders a duty, and accepting a bid beneath the company’s own standalone value would hand shareholders less than they already hold by doing nothing. No board can defend that, and few would survive trying. That makes $90 billion a line with teeth, not a wish.

What makes the floor robust is what sits inside it. The $90 billion is not a snapshot of today’s revenue; it already includes roughly $35 billion of platform option value, the future programs the delivery engine will keep producing. Staying independent means keeping all of that upside for existing shareholders. A buyer must therefore pay at least $90 billion simply to match what Arrowhead’s owners already possess by doing nothing at all. Anything less asks them to sell the future at a discount, and they should not.

Arrowhead also feels none of the pressure its suitors feel, and that is the heart of the matter. It is not a distressed seller. It has an approved drug generating revenue, a deep partnered pipeline throwing off milestones, and the runway to keep building. The whole thesis of this series is that the buyers are cornered by their patent cliffs; the seller is cornered by nothing. A party under a clock negotiating against a party with no clock does not set the price low. That asymmetry is precisely what lets Arrowhead hold its floor and push the final number up toward the buyers’ ceilings rather than down toward its own.

The floor is not even static. A successful first readout from the brain program would lift the platform’s standalone value, and with it the price below which Arrowhead refuses to sell. Time and data work for the seller. The same event that tightens the screws on the buyers raises Arrowhead’s walk-away, which is itself a reason a confident board would wait rather than take an early offer.

Put both sides on the table and the deal space is clear. Arrowhead should not sell below roughly $90 billion, while every buyer ceiling, the $160 to $205 billion figures from the bidding section, sits far above that floor. The zone of a possible deal is therefore wide, and with three motivated buyers competing inside it, the clearing price is pushed up through that zone rather than down to its floor. The realistic $90 to $150 billion sale range is simply where a rising seller floor and a contested set of buyer ceilings are most likely to meet. The $90 billion anchors the bottom of that range for one reason: it is the least Arrowhead should ever accept to give up its independence.

What changes if the price changes?

A fair question is how sensitive all of this is to the price. Figure 4 redraws the grid across the realistic sale range, at $150 billion, $120 billion, and $90 billion. Watch what moves and what holds still.

Figure 4: The grid across the realistic sale range

The payoff grid recalculated at $150 billion, $120 billion, and $90 billion. The red losses are identical across all three; only the green gains change as the price moves.

The red squares never change. The damage a rival does by owning the platform has nothing to do with what was paid for it, so the cost of losing is identical across all three panels. Only the green gains move, and watching them move across the range is instructive.

At $90 billion, the low end, every buyer wins handsomely: Novartis nets $80 billion, Roche $70 billion, even Lilly $50 billion. At $120 billion the gains shrink but stay clearly positive for all three. At $150 billion, the top of the range, something telling happens. Lilly’s own square turns red, because $150 billion now exceeds what Arrowhead is worth in Lilly’s hands. The instinct is to say Lilly should walk away, and the instinct is wrong. An overpriced win at $150 billion costs Lilly about $10 billion, while letting Novartis take the asset instead costs it $20 billion, so Lilly keeps bidding rather than accept the worse outcome. That red square is the winner’s curse made visible: a forced move can push a buyer past the point where winning makes sense on its own, purely because losing is worse.

That dynamic decides how an auction would actually end. As the price climbs past the top of the realistic range, the weakest-fit buyer drops out first, Lilly at its $160 billion ceiling, leaving the two most motivated, Novartis and Roche, to set the final price. The grid shows the outcome at each fixed price; how high each would actually go is the separate question answered by the floors and ceilings above.

Why not build, license, or buy someone else?

A fair challenge runs through all of this: if these companies need RNAi and brain delivery, why must they buy Arrowhead? They could build the capability themselves, license a single program, or buy a different company. The honest answer is that each alternative is weaker, and seeing why strengthens the case.

Building takes time the cornered companies do not have. Delivering RNA into tissues beyond the liver, and especially into the brain, has taken Arrowhead more than a decade of chemistry. A Novartis staring at its cliff in 2026 cannot wait out a ten-year internal program.

Licensing one program solves one problem, not the strategic one. A license gives a buyer a single drug on someone else’s terms; it does not hand over the platform, the delivery toolkit, the dozens of future programs, or the people who built them, the scientists who have solved one hard delivery problem after another, pushed RNAi into tissue after tissue beyond the liver, and engineered trigger chemistry at the leading edge of the field. A license leaves all of that, and the asset itself, on the table for a rival. The Sarepta and GSK deals with Arrowhead show that licensing happens, yet none of them removed Arrowhead as a target.

Buying a different RNAi company is the strongest objection, and the obvious candidate is Alnylam. Here the distinction matters. Alnylam is a finished franchise: profitable, with 2026 product revenue guided to roughly $4.9 to $5.3 billion, anchored by its heart drug, and valued near $42 billion before any premium. It is the better company to own outright, a mature and cash-generative business. It is the worse fit for this particular need, because its delivery is concentrated in the liver, it carries less of the brain and extrahepatic optionality a cliff-facing buyer is reaching for, and it is already entangled with two of the three buyers, since Novartis commercializes its Leqvio and Roche partners on another of its drugs. Arrowhead is the engine: broader tissue reach, a real path into the brain, a deep cardiometabolic pipeline, and far more future revenue still ahead of it. That does not make Arrowhead cheaper. Its market value is a fraction of Alnylam’s today, near $12 billion against $42 billion, yet the strategic price it would command, the $90 to $150 billion in this note, sits above what Alnylam would cost to acquire. A buyer pays more for Arrowhead precisely because it is buying the future and the breadth rather than a single mature franchise. Alnylam is the better company to own, Arrowhead the better company to acquire.

Can they actually pay, and clear the regulators?

A ceiling no one can fund or clear past regulators is not a real ceiling, so two practical checks matter. On the money, all three can write the check. Lilly, valued over $1.1 trillion, has by far the most room. Roche is large and cash-generative across drugs and diagnostics. Novartis carries more debt, with net debt around $22 billion after recent moves, yet it has shown it will borrow for the right asset, and the Pfizer purchase of Seagen showed a buyer raising roughly $31 billion in fresh debt for a platform it wanted. A price in the range discussed here is large, yet within reach for each, especially with a mix of debt and stock.

On the regulators, the path looks clearer than for a typical mega-merger. Arrowhead’s only marketed product today is plozasiran, a therapy for a rare triglyceride disorder, and none of the three buyers sells a competing product in that small market, so a deal eliminates almost no existing competition, which is the usual antitrust trigger. The closest concern is overlap inside a single disease area, for instance Novartis already holding an RNAi cholesterol drug, and the standard remedy there is a narrow divestiture rather than a block. Pfizer cleared its Seagen deal by giving up one product’s United States royalties to satisfy the regulator. The lesson is that these deals get done, sometimes with a minor concession, rather than stopped.

How firm are these numbers

Honesty matters here. The patent-cliff figures behind Figure 1 are the most solid, drawn from public sales and known expiry dates, though they remain projections of how fast sales erode. The gains rest on two assumptions you can change: the $90 billion baseline value, whose softest piece is the platform option value broken out in Figure 3, and the price, which Figure 4 flexes across the realistic range. Both move the green numbers dollar for dollar. The competitive-damage figures in the red squares are the softest of all. Their relative size is well reasoned, with Roche losing most to a Novartis win, yet the exact dollars are estimates and should be read as approximate rather than precise. To make that concrete, the competitive-damage cells are best read with a band of roughly 30 percent either way, so Roche’s $45 billion loss to a Novartis win is better understood as a range from about $30 billion to $60 billion. One thing the model now gets right by construction: it counts each piece of value only once, never as both a gain and a loss.

What would break this thesis

Honest analysis names what would prove it wrong, and several things would. The clearest is the science. Arrowhead’s brain program, ARO-MAPT, has not yet shown that it works in people, and a clear failure at its first human readout would knock out the most valuable part of the platform and deflate the urgency for the brain-focused buyer, Roche above all.

A rival platform could leap ahead. If another company demonstrated cheaper or better delivery into the brain or other hard tissues, Arrowhead’s scarcity, the very thing that makes it worth fighting over, would erode.

The buyers could simply decline. A forced move is a claim about incentives, not a guarantee of behavior. Boards delay, balk at premiums, and sometimes choose to build despite the logic, so the thesis predicts pressure, not certainty.

Arrowhead could take itself off the table. A large financing, a transformational partnership, or a clear statement of intent to stay independent would signal that management does not mean to sell, which would defer the whole question. Watching for those signals is part of testing the thesis rather than merely asserting it.

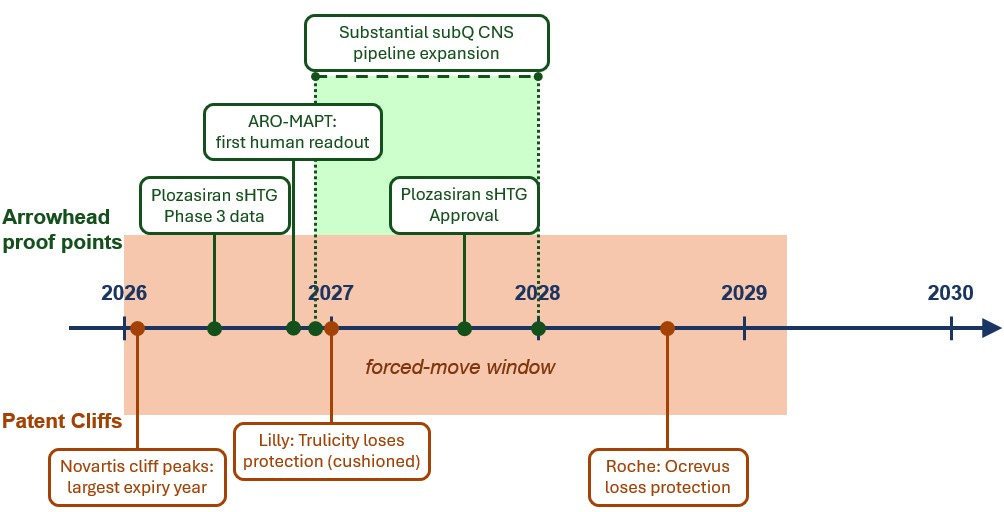

The clock: when the move gets forced

A forced move needs a trigger, and the triggers are dated. Figure 5 lines them up.

Figure 5: Two clocks running at once

The cliff clock below the line and Arrowhead’s proof points above it. The shaded window is where a revenue hole and a platform proof point overlap.

Two clocks run at the same time. The cliff clock is already ticking for Novartis, whose largest expiries land in 2026, and it builds toward Roche as Ocrevus rolls off around 2028 and 2029. Arrowhead’s side runs hot in the very same window: the sHTG Phase 3 data land in 2026 and a plozasiran sHTG approval could follow in 2027, while the first human readout from the brain program, the event most likely to convert the platform from promise into proof, is also expected in late 2026. That readout is a gate, not a footnote: it opens a substantial CNS pipeline expansion that Arrowhead has slated to begin at the end of 2026 and run through 2027, so it does not add a single proof point; it opens a portfolio. When a cluster of proof points on Arrowhead’s side meets a revenue hole on a buyer’s side, the pressure stops being theoretical. That overlap, more than any single number in this note, is what would set a forced move in motion.

What it all means

One contrast ties it all together. Arrowhead trades near $12 billion today, yet each of the three buyers could rationally justify paying somewhere between $160 and $205 billion, well over ten times that, once the cost of letting a rival win is counted. That gap, between a market price set by today’s results and a strategic price set by tomorrow’s threat, is the entire point of the Forced Move thesis. When all three would pay far more than the asset is likely to clear for, the result is not a quiet negotiation. It is a bidding war.

The grid does not promise that any deal will happen. Real acquisitions turn on personalities, regulators, balance sheets, and timing that no model captures. What it shows is why the pressure exists, why no company can comfortably sit out, and how the squeeze falls differently on each: Novartis cornered first by the timing of its cliff, Roche most threatened by a specific rival, Lilly the most able to wait. Chess players have a name for the moment when every comfortable option has quietly vanished and only one move keeps you in the game. They call it the forced move. The board is nearly set, and the clocks are running. No one at this table wants to pay $100 billion for a company the market prices at $12 billion. That, precisely, is why one of them will.

A Note on Supporting Independent Research

If this note has been valuable to you, whether it shaped your thinking, validated your conviction, or simply saved you the time of doing this work yourself, a voluntary contribution is genuinely appreciated and directly funds the next paper.

For individual investors and readers

Any amount you feel reflects the value you received is welcome and meaningful. A contribution in the range of what you might pay for a single premium research report is a thoughtful gesture that makes a real difference.

For family offices, investment funds, hedge funds, and research platforms

This paper is the caliber of work that institutional research desks bill significant retainers to produce. If your team referenced it, distributed it internally, or used it to inform a position, a suggested contribution of $1,000 reflects the professional value of the analysis, though any amount is meaningful. Your support makes it possible to continue publishing at this level without a paywall that limits the reach of the ideas. If your organization requires an invoice to process a payment, please reach out directly at bioboyscout@gmail.com and one will be provided promptly.

There is no obligation and no expectation. This is purely a thank you for work that meant something to you.

Zelle: (847) 227-7909

PayPal: paypal.me/bioboyscout

Thank you for reading, and for being part of a community that takes this thesis seriously.

— Robert Toczycki | BioBoyScout

Important Risks, Disclosures, & Disclaimers

The author, Robert Toczycki (aka BioBoyScout), certifies that:

all views expressed in this note accurately reflect his personal opinions about the topic discussed;

he was not compensated in any form for producing this note; and

he has not received and does not receive compensation from Arrowhead Pharmaceuticals.

This note reflects the author’s personal opinions, is for informational purposes only, and is not investment advice. The figures shown are modeled estimates meant to illustrate a strategic argument, not forecasts of any specific transaction or price. It does not constitute investment advice, a solicitation to buy or sell securities, or a guarantee of future results. The author holds a long position in Arrowhead common stock. Arrowhead Pharmaceuticals (ARWR) is a publicly traded company; investments in its shares involve material risks, including the risk of total loss.

About the Author

Robert Toczycki is an independent analyst and registered US Patent Attorney with a JD, an Executive MBA completed at the top of his class, and a BS in Mathematics and Computer Science from the University of Illinois at Urbana-Champaign. He has a deep passion for financial analysis, particularly identifying valuation discrepancies and demonstrating them through rigorous, data-driven research and solid analytics.

Comments or questions: bioboyscout@gmail.com.

Copyright © 2026, BioBoyScout. All Rights Reserved.

I note that Biogen are releasing P2 data for their Tau targeting ASO at the forthcoming AAIC meeting. There may be some (albeit limited) read through to the Arrowhead asset.