Zero

JPMorgan says Arrowhead's brain platform is a major event. Its own price target values it at nothing. The gap between what the sell side says and what it models is the whole investment case.

Robert Toczycki, JD, MBA

bioboyscout.com

bioboyscout@gmail.com

847.227.7909

X: @BioBoyScout

Every so often an argument arrives fully assembled, made by someone with no interest in making it. This is one of those. JPMorgan published a note last week reiterating an Overweight rating on Arrowhead with a price target of $88. Inside that note is a sentence that should stop any careful reader, and a table that contradicts it.

The sentence says the brain program is the first asset in Arrowhead’s pipeline aimed at crossing the blood-brain barrier to reach the clinic, and that management expects a substantial expansion of the entire central nervous system pipeline if its first readout is encouraging. The table says that program is worth nothing.

Where the $88 comes from

A price target is not a slogan. It is arithmetic, and the arithmetic is published. Here is how JPMorgan builds its $88.

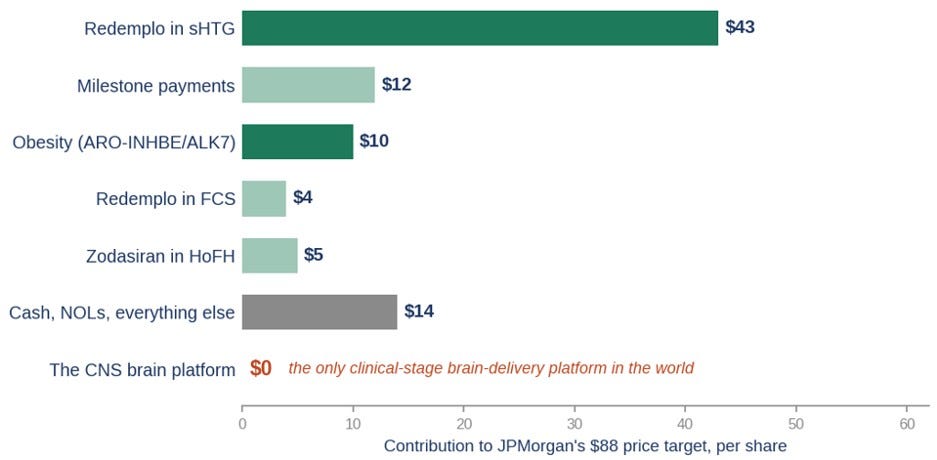

Figure 1: What JPMorgan’s $88 is made of

The stated components of JPMorgan’s December 2026 price target for Arrowhead, per share. The brain platform, the company’s most differentiated asset, appears nowhere. Composition from JPMorgan’s published note, July 2026.

Roughly $43 a share for the approved triglyceride drug in its larger indication. About $4 for the same drug in the rare disease where it is already approved. Around $5 for a second cardiometabolic drug, about $10 for the obesity programs, and roughly $12 for potential milestone payments from partners. The rest is cash, tax assets, and an unspecified remainder labeled pipeline value.

Read that list again and note what is missing. The delivery platform that lets Arrowhead put gene-silencing drugs into tissues nobody else can reach carries no line. The brain program, ARO-MAPT, carries no line. The bench of central nervous system targets behind it carries no line. The platform is not modeled conservatively. It is not modeled at all.

The contradiction, stated plainly

Hold the two halves of that note side by side. In the text, JPMorgan tells clients that the brain readout is important derisking, that it is the first blood-brain-barrier asset the company has put into humans, and that a good result triggers a substantial pipeline expansion beginning at the end of 2026. In the model, the same firm assigns that asset, that platform, and that expansion a value of zero.

Both cannot be right. Either the platform matters, in which case the price target is missing its most important input, or it does not matter, in which case the note should not describe it as a major derisking event. What JPMorgan has actually published is a valuation of Arrowhead as a cardiometabolic company that happens to own a brain platform for free.

This is not a criticism of the analyst. It is how sell-side models work, and it is precisely the mechanism I have been describing for months. A discounted cash flow can only value what it can forecast, and it cannot forecast a platform whose first human data does not exist yet. Faced with an unproven asset, the model does the only thing it knows how to do. It assigns zero and waits. The result is a price target that captures the company Arrowhead is today and none of the company it is becoming.

Zero is not the conservative answer

The defense an analyst would offer is that a model cannot value what has not read out. Set that defense against the same analyst’s own arithmetic. Roughly $10 of the $88 sits on the obesity programs, which is the right call, since those programs have already produced human data, meaningful reductions in visceral, total, and liver fat, and doubled weight loss in combination with tirzepatide. About $12 sits on milestone payments that hinge on other companies’ trials. Both are estimates of things not yet certain, and the analyst is right to make them, because making them is the job. The model is entirely willing to price an early clinical asset on a probability, right up to the moment it reaches the brain platform, where it suddenly assigns nothing. That is not caution. It is selective, and the selection lands on the single most valuable asset in the company.

The point cuts deeper than one note, because risk-adjusting unproven assets is not something biotech analysts occasionally do. It is the job. In most industries an analyst forecasts revenue that already exists. In biotechnology almost nothing exists yet, so the entire discipline is built on putting numbers on things that have not happened. Probability of technical success, phase-by-phase attrition rates, risk-adjusted net present value, probability-weighted peak sales: these are not exotic instruments. They are the daily vocabulary of the profession, and analysts rightly take pride in wielding them. Assigning a defensible number to a deeply uncertain asset is the craft itself.

A zero, in any case, is not a number the model produced. It is the number that appears when nobody enters one. There is a difference between running the calculation and arriving at something small, which is rigorous, and never creating the line item at all, which is an absence wearing the costume of an estimate. A conservative analyst would take a low probability of success, apply a modest value, and publish a small figure. That is defensible and it is honest work. Zero is not conservatism. Zero is the only output that requires no analysis whatsoever.

There is a cost to that absence, and it is not merely academic. A price target is supposed to be a forecast, which means it should already carry the probability-weighted value of events that are foreseeable. The brain readout is about as foreseeable as an event in this business gets. It is scheduled, the company has said when to expect it, the bar for success is public, and the consequences of clearing that bar are estimable within a range. A model that carries no expectation for it is not forecasting the future. It is photographing the present and putting a future date on the frame.

Notice the date on that frame. The price target runs to December 2026. The readout arrives in the fall. The target is therefore dated after the single most important event of Arrowhead’s year, and priced as though that event will not occur.

To be clear about what is and is not being argued. A stock should move sharply when a great deal is learned, and a large repricing after a genuine binary readout is the correct outcome, not a failure. What should not happen is that the repricing comes as news to the model. The purpose of risk-adjusting an unproven asset is to hold, today, a considered view of what tomorrow might bring, so that when tomorrow comes the analyst is updating a number rather than inventing one, and is not blindsided by an event that was on the calendar all along.

The fair objection is that sell-side convention often does keep early-stage and preclinical assets out of a formal discounted cash flow, handling them qualitatively in the text instead. That convention is real, and in most cases it is harmless. It stops being harmless when the excluded asset is the most valuable thing the company owns, and when the same analyst, in the same document, calls it major derisking. At that point the convention is not prudence. It is the reason the mispricing exists.

Recognize what a zero actually asserts. It is not a shrug, and it is not caution. Written down, a zero is a specific and aggressive claim: probability of success multiplied by value equals nothing. Not small. Not uncertain. Nothing. To hold that view of Arrowhead’s brain platform, an analyst must believe either that ARO-MAPT has essentially no chance of working, or that a proven subcutaneous route into the human brain would be worth nothing once it did. No analyst would say either sentence out loud, and yet the model says both.

The minimum honest answer is not a zero. It is a range. Take a probability of success, take a value if it works, multiply, and publish the number. That is the ordinary machinery of sell-side valuation, applied everywhere else in the very same note. The anchors for that estimate are not hard to find. What informed buyers have actually paid for brain access, examined below, sets a floor, and discounting those prices aggressively still does not get you to zero.

The asset is not undifferentiated guesswork either. Arrowhead has spent years removing risk from this program in ways an analyst can actually see: primate data showing roughly 50 to 60 percent knockdown in the brain sustained for months, an approved trial enrolling patients today, a partner who paid real money for a piece of the platform, and a patent estate built around the delivery route itself. The target has now been derisked as well, by someone else’s capital. Biogen’s diranersen has shown that lowering tau in the human brain produces measurable clinical benefit, which removes the most fundamental question hanging over ARO-MAPT: whether the thing it is aimed at is worth aiming at. The platform is more derisked today than it was on the day the price target was published. The valuation assigned to it has not moved.

Why this is the strongest evidence yet

For months these white papers have argued that the market prices Arrowhead’s drugs and ignores its platform. That was an assertion. This is a receipt.

Consider the source. This is not a bearish analyst reaching for reasons to be negative. It is a bulge-bracket firm that rates the stock Overweight, that recommends buying it, and that in the same document praises the brain program in the warmest terms available. Even in the mouth of a bull, the platform is worth nothing. If the most enthusiastic sell-side model in the room carries a zero in that line, ask what is actually inside the roughly $72 a share the market is paying today.

The answer is: the triglyceride franchise, the obesity programs, some milestones, and the cash. That is the whole stock. Everything these white papers have called the crown jewel, the delivery technology, the brain pipeline, the strategic scarcity that makes three large pharmaceutical companies pay attention, is being handed to buyers at no charge.

What the platform is worth to someone who has to buy it

Set the models aside and look at what strategic buyers actually pay, because they cannot afford the luxury of a zero. Novartis committed $200 million upfront and as much as $2 billion for a narrow slice of Arrowhead’s neurology work, and it did so while already owning its own liver-targeted RNAi drug and while cheap liver-focused licensing deals were freely available. It was not buying the cardiometabolic pipeline that makes up the whole of JPMorgan’s price target. It was buying access to the brain.

BioArctic makes the point sharper still. With a blood-brain-barrier delivery technology but no approved drug of its own riding on it, it has signed four separate agreements in about two years, with Bristol Myers, Novartis, Lilly, and Eisai, each worth from hundreds of millions to well over a billion dollars, for nothing more than a way across the barrier. Four large pharmaceutical companies have paid, repeatedly and in public, simply for the right to try. Arrowhead has the only platform of its kind already in the clinic, a brain drug dosing humans today, and a partner that has committed as much as $2 billion to one corner of it. Whatever the right number is, the observed evidence says it begins in the billions. Zero is not a conservative estimate of it. Zero is a placeholder for a number the model cannot generate.

Sarepta is the third data point, and it tests a different claim than the other two. Novartis and BioArctic price the value of reaching the brain. Sarepta prices the value of the platform itself, its capacity to keep producing licensable programs across tissues. In late 2024 Sarepta licensed a suite of Arrowhead’s clinical and preclinical programs spanning muscle, lung, and the central nervous system, including central nervous system targets in Huntington’s disease and the spinocerebellar ataxias. It paid $825 million immediately, $500 million in cash plus a $325 million equity stake taken at a 35 percent premium, committed a further $250 million over five years, and put up to roughly $10 billion in milestones behind the collaboration, with the right to commission six more targets from the platform on demand.

Read what that structure actually says. A sophisticated partner did not buy one drug. It bought standing access to the factory, the right to keep pulling new programs off Arrowhead’s delivery platform for years. That is the precise asset JPMorgan labels pipeline value and scores at nothing. Sarepta named the reason itself, calling Arrowhead’s approach to crossing the blood-brain barrier with a subcutaneous shot a potential paradigm shift for the central nervous system programs it was licensing. The acquiring partner identified, by name, the capability the model refuses to value. Note the honest limits: several of these programs are early, the headline figure is milestone-heavy rather than banked, and Sarepta has had its own turbulence, so the realized total will depend on execution. None of that touches the point, because the point is not what Sarepta will eventually pay. It is what an informed party agreed the platform was worth paying for in the first place, and that number was not zero. It was among the largest platform-licensing commitments in the sector.

The event that removes the excuse

Here is why this matters now rather than in the abstract. A model can carry a zero only while the asset remains unproven. The moment human data exists, the zero becomes indefensible, and every analyst carrying one has to replace it with a real number.

Arrowhead’s first human brain readout is expected late in the third quarter or early in the fourth. The bar is public: diranersen, the competing intrathecal drug, lowered tau in the spinal fluid by roughly 50 to 60 percent, and Arrowhead management has said it is looking for a comparable reduction in its own study as the mark of success. Its primate data already sits in that range, and its modeling projects sustained knockdown of 50 to 70 percent on quarterly dosing.

Consider what a positive result would do to a model like JPMorgan’s. It would not adjust an assumption. It would force the creation of a line item that does not currently exist, in a valuation where the largest single component is a triglyceride drug. Analysts do not re-rate gently when they have to build a new section of the model from nothing. That is the mechanical path from $88 to something that starts with a different digit.

What would make this wrong

Honesty requires the obvious caveat. The zero is only wrong if the platform works. If the brain readout disappoints, if the knockdown comes in well below the 50 to 60 percent bar, then the models were right to assign nothing, and the stock is roughly worth what the cardiometabolic franchise is worth. That is the risk, stated without varnish.

Note the asymmetry, though. If the platform fails, the market was correct and the stock is priced about right. If the platform works, the market is carrying a zero on the most strategically scarce asset in the sector, and it has to fix that in a hurry. Losing is being right about the price you already paid. Winning is a repricing that no model in the room is currently prepared for.

The hanging piece

Chess has a word for this. A piece is hanging when it sits on the board undefended, fully available for capture, and the player who should be watching it simply has not noticed. The piece has lost none of its value. Nobody is counting it.

That is what a zero in a valuation model actually describes. It does not say the brain platform is worthless. It says nobody has been forced to put a number on it, so the line stays empty and the position looks quieter than it is. The asset sits there in plain sight, undefended, worth exactly what it was worth before anyone bothered to look.

The trouble with a hanging piece is that it does not stay hanging. Somebody eventually looks at the board and counts it. It might be an analyst, obliged to build a line item after a readout leaves no excuse for the zero. It might be a strategic buyer who has been counting all along, which is what Novartis was doing when it wrote a check for the brain while the models were writing nothing.

What it all means

The most valuable thing Arrowhead owns does not appear in the arithmetic of the bank that recommends buying it. That is the entire thesis in a sentence, and this time it is not a claim from a letter with a position. It is published, sourced, and reiterated with an Overweight rating.

The market is not wrong about the triglyceride drug. It is not wrong about obesity, or the milestones, or the cash. It is simply not counting the road into the brain, because nothing has yet compelled it to. A price target is a bet on the company you can already see. The whole argument for owning this one rests on the company nobody has priced yet.

In chess, a piece that nobody defends is not a piece without value. It is a piece about to change hands.

A Note on Supporting Independent Research

If this note has been valuable to you, whether it shaped your thinking, validated your conviction, or simply saved you the time of doing this work yourself, a voluntary contribution is genuinely appreciated and directly funds the next paper.

For individual investors and readers

Any amount you feel reflects the value you received is welcome and meaningful. A contribution in the range of what you might pay for a single premium research report is a thoughtful gesture that makes a real difference.

For family offices, investment funds, hedge funds, and research platforms

This paper is the caliber of work that institutional research desks bill significant retainers to produce. If your team referenced it, distributed it internally, or used it to inform a position, a suggested contribution of $1,000 reflects the professional value of the analysis, though any amount is meaningful. Your support makes it possible to continue publishing at this level without a paywall that limits the reach of the ideas. If your organization requires an invoice to process a payment, please reach out directly at bioboyscout@gmail.com and one will be provided promptly.

There is no obligation and no expectation. This is purely a thank you for work that meant something to you.

Zelle: (847) 227-7909

Thank you for reading, and for being part of a community that takes this thesis seriously.

— Robert Toczycki | BioBoyScout

Important Risks, Disclosures, & Disclaimers

The author, Robert Toczycki (aka BioBoyScout), certifies that:

all views expressed in this note accurately reflect his personal opinions about the topic discussed;

he was not compensated in any form for producing this note; and

he has not received and does not receive compensation from Arrowhead Pharmaceuticals.

This note reflects the author’s personal opinions, is for informational purposes only. It does not constitute investment advice, a solicitation to buy or sell securities, or a guarantee of future results. Figures cited from JPMorgan’s published research note dated July 2026 and from company disclosures. The author holds a long position in Arrowhead common stock. Arrowhead Pharmaceuticals (ARWR) is a publicly traded company; investments in its shares involve material risks, including the risk of total loss.

About the Author

Robert Toczycki is an independent analyst and registered US Patent Attorney with a JD, an Executive MBA completed at the top of his class, and a BS in Mathematics and Computer Science from the University of Illinois at Urbana-Champaign. He has a deep passion for financial analysis, particularly identifying valuation discrepancies and demonstrating them through rigorous, data-driven research and solid analytics.

Comments or questions: bioboyscout@gmail.com.

Copyright © 2026, BioBoyScout. All Rights Reserved.